TL;DR:

- Commercial property assessments estimate taxable value, influencing property tax liabilities but differ from market value. Owners can challenge assessments by understanding valuation methods, deadlines, and how property conditions like deferred maintenance impact evaluated worth. Proper documentation and proactive inspections can significantly improve the chances of lowering assessed values and managing investment risks.

A commercial property assessment is an official government estimate of your property’s taxable value, used to calculate how much property tax you owe each year. This figure is not the same as market value, and confusing the two costs investors real money. Understanding commercial property assessments means knowing how assessors arrive at that number, when you can challenge it, and what physical conditions on your property can shift the outcome. The three core valuation methods, the appeal window, and the distinction between assessed and taxable value are the tools every commercial owner needs to manage tax exposure and protect returns.

What valuation methods drive commercial property assessments?

Commercial property assessments primarily use three approaches: the income approach, the sales comparison approach, and the cost approach. Each method suits different property types, and assessors may apply one or blend all three depending on the asset class and available data.

The Income Approach is the most common method for income-producing properties like office buildings, retail centers, and apartment complexes. The assessor estimates Net Operating Income (NOI) and divides it by a capitalization rate to produce a value. Cap rates ranged 5%–8% in 2025 across most commercial sectors. That range matters because a small shift in the cap rate produces a large swing in assessed value. A property generating $500,000 in NOI assessed at a 5% cap rate is valued at $10 million. At 6%, that same property drops to $8.3 million. The cap rate is often the single most contestable assumption in the entire process.

The Sales Comparison Approach works best when there are enough recent, comparable sales in the market. The assessor identifies arm’s-length transactions for similar properties and adjusts for differences in size, condition, location, and lease terms. This method is most reliable in active markets with consistent transaction volume. In slower markets or for specialized properties, comparable sales are scarce, which weakens the method’s accuracy.

The Cost Approach estimates what it would cost to replace the building at current construction prices, then subtracts depreciation for age, wear, and functional obsolescence. This approach is most useful for newer buildings or special-use properties like hospitals or schools where income data and comparable sales are limited.

| Approach | Best For | Key Input |

|---|---|---|

| Income | Retail, office, multifamily | NOI and capitalization rate |

| Sales Comparison | Active markets with recent sales | Comparable transaction data |

| Cost | New or special-use properties | Replacement cost minus depreciation |

Pro Tip: If your property is assessed using the income approach, request the assessor’s cap rate assumption. That single number is often the most effective point of challenge in a formal appeal.

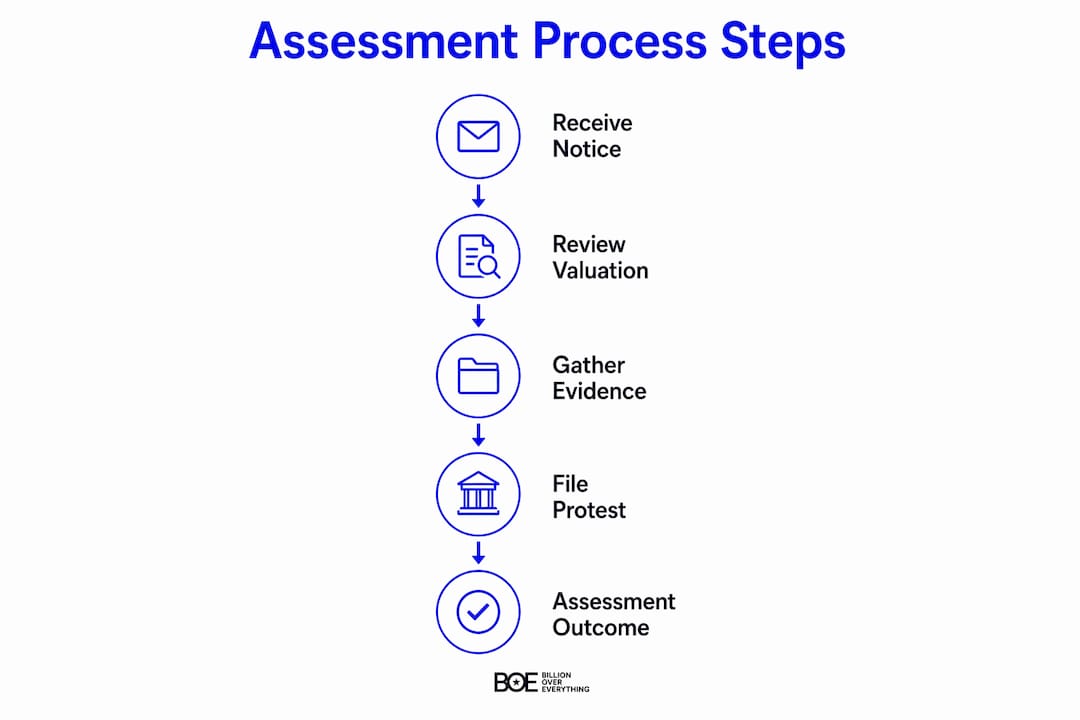

How does the assessment process work, and when are deadlines?

The assessment cycle follows a predictable pattern, though timing varies by state and county. Assessors conduct mass appraisals, meaning they value large groups of properties using standardized models rather than individual inspections. This efficiency creates inaccuracy, and that inaccuracy is your opportunity.

Here is how the process typically unfolds:

- Assessment date. The assessor establishes a value as of a specific date, often January 1 of the tax year. All evidence used in an appeal must reflect conditions on or before that date.

- Notice of Appraised Value. Owners receive a mailed notice showing the new assessed value. In Michigan, notices often arrive in February, and protest windows commonly last 30 days. Missing this window forfeits your right to appeal for that cycle.

- Informal review. Most jurisdictions allow an informal meeting with the assessor’s office before a formal protest. Bring documentation. Many disputes resolve here without a formal hearing.

- Formal protest or appeal. If the informal review fails, you file a formal protest with the appraisal review board or equivalent body. Deadlines are firm. Late filings are rejected without exception.

- Tax bill. Once the assessed value is finalized, the jurisdiction applies the local mill rate to calculate your tax bill. One mill equals $1 per $1,000 of taxable value, so a $5 million taxable value at 20 mills produces a $100,000 annual tax bill.

Pro Tip: Calendar your Notice of Appraised Value arrival date every year. Set a reminder 10 days before the protest deadline. The window closes fast, and extensions are rarely granted.

What is the difference between assessed value, market value, and taxable value?

These three terms describe three different numbers, and conflating them leads to poor tax strategy. Market value is the price a willing buyer pays a willing seller in an arm’s-length transaction. Assessed value is the government’s estimate of that market value, often calculated using mass appraisal models. Taxable value is what you actually pay taxes on, derived from assessed value after applying an assessment ratio.

The assessment ratio is the percentage of market value that becomes taxable. Ohio, for example, taxes commercial property at 35% of market value as the taxable value. A property with a $2 million market value carries a $700,000 taxable value in Ohio. That ratio varies significantly by state and sometimes by property classification within a state.

Here is how the three values relate in practice:

- Market value: What the property would sell for today in an open market transaction.

- Assessed value: The assessor’s estimate, which may be equal to market value or a fraction of it depending on jurisdiction.

- Taxable value: Assessed value multiplied by the assessment ratio, then used to calculate the actual tax bill.

Owners sometimes assume that if their assessed value is lower than what they paid, they have no grounds for appeal. That logic is flawed. The relevant question is whether the assessed value accurately reflects current market value given the property’s actual condition, vacancy, and income. A property purchased at peak pricing may now carry an assessed value that still exceeds its current market reality.

Formal appraisals provide objective, data-driven valuation critical for lending, legal, and investment decisions. They cover income potential, location, condition, and comparable sales. A formal appraisal from a licensed MAI appraiser is the strongest evidence you can bring to an appeal hearing.

How can owners use assessment insights to manage investment risk?

Assessors rely on mass appraisal without accounting for property-specific issues like deferred maintenance or high vacancy, which creates real appeal opportunities. The gap between what the assessor assumes and what your property actually produces is where over-assessments live.

Common factors assessors miss or underweight include:

- Deferred maintenance. A roof at the end of its service life, aging HVAC units, or deteriorating parking surfaces reduce market value. Assessors working from public records rarely capture this. A deferred maintenance assessment documents these conditions with specificity, giving you evidence that holds up in a hearing.

- Vacancy and lease terms. An assessor using market-rate occupancy assumptions on a property running 30% vacant will over-value the income stream. Actual rent rolls and current lease abstracts correct this.

- Market lag. Assessment cycles lag behind market changes, so assessments may not reflect recent market declines. When office values drop under pressure while assessments remain anchored to prior-year peaks, the over-assessment is real and documentable.

- Asset class divergence. Office values face pressure while industrial and multifamily assets often perform better. Sector-specific conditions matter when reviewing whether the assessor’s assumptions fit your property type.

Owners who present asset-class specific evidence during appeals, rather than broad market arguments, consistently produce better outcomes. The assessor’s model is built on averages. Your appeal succeeds when you replace those averages with your property’s actual numbers.

Pro Tip: Pull your property’s rent roll, current lease abstracts, and a recent income and expense statement before reviewing your assessment notice. If the assessor’s assumed NOI is higher than your actual NOI, you have a direct, quantifiable basis for appeal.

To assess commercial property condition accurately before an appeal, document every deferred maintenance item with photographs, contractor estimates, and inspection reports. That paper trail is what converts a general complaint into a credible reduction request.

Key takeaways

Accurate commercial property assessment knowledge directly reduces tax liability and protects investment returns by exposing the gap between assessor assumptions and actual property conditions.

| Point | Details |

|---|---|

| Three valuation methods | Income, sales comparison, and cost approaches each suit different property types and data availability. |

| Cap rate is contestable | A small cap rate change can shift assessed value by millions; always request the assessor’s assumption. |

| Deadlines are firm | Protest windows often last just 30 days after the notice arrives; missing them forfeits your appeal rights. |

| Assessed value differs from taxable value | Assessment ratios like Ohio’s 35% rule convert assessed value into the taxable figure used for your tax bill. |

| Deferred maintenance creates appeal grounds | Assessors miss property-specific issues; documented condition problems support a formal value reduction. |

What i’ve learned watching assessors miss the real story

After years of walking commercial properties in the Mid-South, one pattern stands out: the assessor’s model and the property’s actual condition rarely tell the same story. We inspect buildings where the HVAC system is two years past its expected service life, the roof has active ponding, and the parking lot is cracking at every joint. The assessor’s record shows a well-maintained commercial asset at full occupancy. The gap between those two pictures is a tax overpayment waiting to be recovered.

The owners who manage this well are not necessarily the ones with the most expensive attorneys. They are the ones who document conditions consistently, understand which valuation method the assessor used, and come to the informal review with specific numbers rather than general frustration. A formal inspection report that itemizes deferred maintenance with cost estimates is more persuasive than any argument made without documentation.

One thing I would push back on in conventional advice: do not wait until you receive a high assessment notice to start building your file. By then, the assessment date has already passed. Conditions documented after the assessment date carry less weight in a hearing. The time to document your property’s condition is before the assessment cycle closes, not after the notice arrives.

— Holly

How Upchurchinspection supports accurate commercial valuations

When your assessment is based on assumptions that do not match your property’s actual condition, a professional inspection report is the most direct way to close that gap. Upchurchinspection provides commercial property condition assessments that document the physical state of major systems including structural components, electrical, plumbing, and HVAC, with the specificity that appraisal review boards and lenders require. For investors managing tax exposure or preparing for an appeal, the benefits of regular inspections extend well beyond purchase due diligence. They create a dated, evidence-based record of your property’s condition that supports every valuation conversation you will have.

FAQ

What is a commercial property assessment?

A commercial property assessment is an official government estimate of a property’s taxable value, used to calculate annual property taxes. It is based on one or more of three valuation methods: income, sales comparison, or cost.

How does assessed value differ from market value?

Market value is what a property would sell for in an open market transaction. Assessed value is the government’s estimate for tax purposes, which may be a fraction of market value depending on the jurisdiction’s assessment ratio.

Can i appeal my commercial property assessment?

Yes. Most jurisdictions allow owners to file a formal protest within a set window, often 30 days after the Notice of Appraised Value arrives. Evidence of deferred maintenance, actual vacancy, and current income data strengthens an appeal.

What is a capitalization rate and why does it matter?

A capitalization rate converts a property’s Net Operating Income into an estimated value. Because cap rates ranged 5%–8% in 2025, even a one-point difference can shift an assessed value by millions of dollars.

Does property condition affect the assessed value?

Assessors using mass appraisal methods often miss property-specific issues like deferred maintenance or high vacancy. Documenting these conditions with a professional inspection report creates grounds for a formal assessment reduction.