TL;DR:

- A Property Condition Assessment evaluates a commercial building’s physical state, identifies urgent repairs, and forecasts long-term capital needs. Conducted according to ASTM standards, it relies on thorough document review and systematic on-site inspections, with clear separation of immediate repairs and replacement reserves. Engaging actively in the PCA process enhances risk management and supports informed investment decisions.

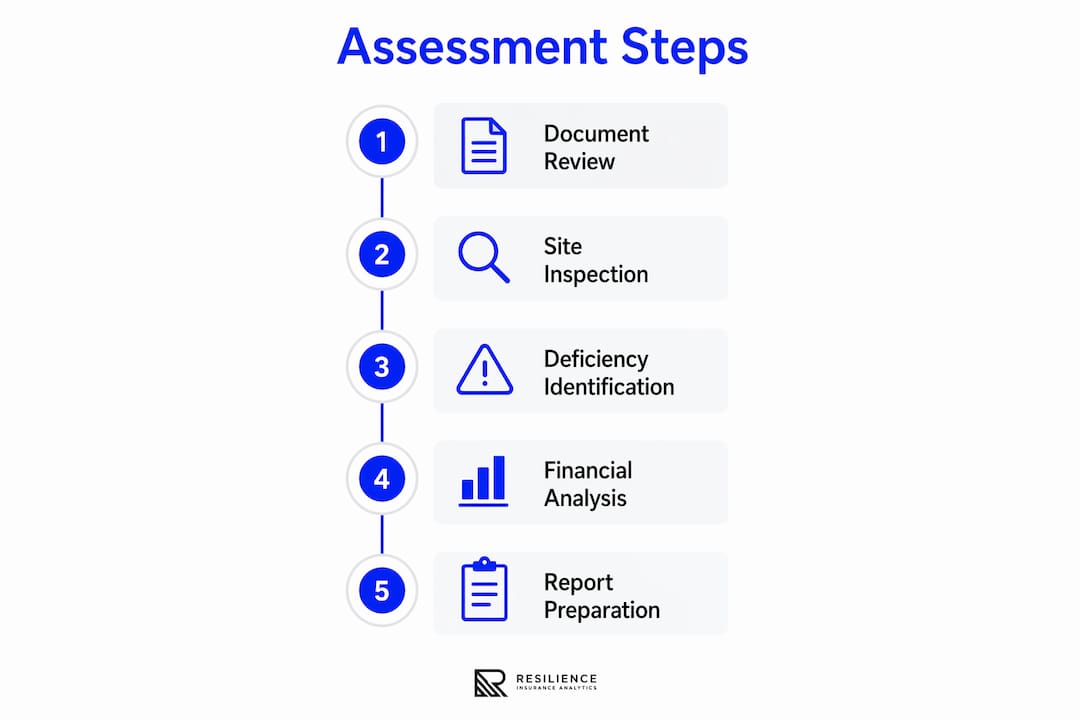

A Property Condition Assessment (PCA) is the structured process investors and business owners use to evaluate a commercial building’s physical state, quantify deferred maintenance, and forecast capital expenditure before a purchase or lease decision. Knowing how to assess commercial property condition correctly separates informed investors from those who inherit expensive surprises. The industry standard governing this process is ASTM E2018, which combines visible-condition observations with cost opinions to support lender and investor decisions. Skip any part of that framework and you are pricing risk on incomplete data.

How to assess commercial property condition: start with documents

The most accurate on-site inspection is only as good as the records that precede it. Construction documents and maintenance records directly inform Remaining Useful Life (RUL) estimates and capital replacement timing, two figures that drive purchase price negotiations and loan structuring. Walking a building without that history is like reading a patient’s chart without their medical records.

Before scheduling the walk-through, request and review the following:

- As-built drawings and original construction documents to understand structural systems, mechanical layouts, and design intent

- Maintenance logs and service records for HVAC units, elevators, roofing, and plumbing to identify deferred maintenance patterns

- Permits and certificates of occupancy to confirm all improvements were legally permitted and inspected

- Past work orders and capital improvement invoices to verify claimed upgrades and assess the quality of prior repairs

- Utility bills for the past 24 months to flag abnormal consumption that may indicate failing systems

Interviews with facility managers and on-site maintenance personnel add a layer of context that no document can fully replace. A maintenance tech who has been servicing the building for eight years knows which HVAC unit runs hot every July and which roof drain backs up after heavy rain. That institutional knowledge shapes where you focus your inspection time.

Pro Tip: Request the maintenance records at least one week before the site visit. Reviewing them in advance lets you build a targeted list of questions and flag systems that warrant closer scrutiny during the walk-through.

What does a systematic on-site visual inspection cover?

A commercial property inspection checklist covers nine primary categories: site improvements, exterior envelope, roofing, structural systems, mechanical systems, electrical systems, plumbing, fire and life safety, and interior conditions. ADA compliance and environmental considerations round out a thorough survey. Missing any one category creates a blind spot that can translate directly into unbudgeted capital costs.

The walk-through follows this sequence for a reason. Moving from exterior to interior and from site to systems mirrors how building failures typically propagate. A drainage problem at the site level, for example, can drive moisture into the foundation before it ever appears as a stain on an interior wall.

- Site and civil improvements: Inspect parking lots, curbs, drainage systems, retaining walls, and exterior lighting for deterioration, settlement, or ADA non-compliance.

- Exterior envelope and windows: Examine cladding, sealants, glazing, and flashing for water intrusion pathways, which are the leading cause of structural damage in commercial buildings.

- Roofing systems: Assess membrane condition, drainage, penetrations, and flashing. Note the installation date and compare it against the manufacturer’s expected service life.

- Structural systems: Look for visible cracking, settlement, or deflection in foundations, columns, beams, and slabs. Flag anything that warrants a structural engineer’s review.

- MEP systems (mechanical, electrical, plumbing): Verify equipment age against published service-life benchmarks, check for deferred-maintenance indicators such as rust, corrosion, or makeshift repairs, and confirm panel capacity.

- Fire and life safety: Confirm sprinkler coverage, fire alarm panel condition, emergency egress, and extinguisher placement against current code requirements.

- Interior conditions: Survey flooring, ceilings, walls, and restrooms for signs of moisture, mold, or deferred cosmetic maintenance that signals neglected upkeep.

The table below summarizes the key systems, common deficiencies, and typical service-life benchmarks that inspectors use as reference points.

| Building system | Common deficiencies | Typical service life |

|---|---|---|

| Built-up or TPO roofing | Membrane blistering, failed flashing | 15 to 25 years |

| HVAC (commercial packaged units) | Refrigerant leaks, heat exchanger cracks | 15 to 20 years |

| Electrical panels and switchgear | Overloaded circuits, outdated breakers | 25 to 40 years |

| Plumbing (cast iron drain lines) | Corrosion, root intrusion | 50 to 75 years |

| Parking lot asphalt | Alligator cracking, failed sealcoating | 20 to 30 years |

Baseline commercial inspections are fundamentally visual and non-invasive. Concealed conditions, such as pipe interiors or wall cavity insulation, fall outside the standard scope unless specialized testing is added by written agreement. Thermal imaging, borescope inspection, and core sampling are common scope expansions that add cost but eliminate guesswork on high-risk systems.

Pro Tip: Always confirm access to all mechanical rooms, roof hatches, and electrical panels before the inspection date. Restricted access on the day of the walk-through forces the inspector to note limitations rather than observations, which weakens the report’s usefulness for negotiation.

How to read and use a PCA report

A PCA report separates findings into two financial categories, and understanding the difference is critical. Immediate repairs and replacement reserves are presented in distinct cost tables that project urgent and long-term capital needs mapped to specific building systems. Treating these two tables as interchangeable is one of the most costly misreads an investor can make.

The Immediate Repairs Table lists deficiencies that require attention within 90 days of closing. These are safety hazards, code violations, or conditions that will worsen rapidly if left unaddressed. A failed fire suppression system, an actively leaking roof membrane, or an electrical panel with evidence of arcing all belong here. This table directly informs your price negotiation or repair credit request.

The Replacement Reserves Table projects capital needs over a 12-year horizon, broken down by building system and year. PCA reports must clearly distinguish between immediate deficiencies and deferred maintenance and provide RUL estimates that are objective and cost-supported. A roof with five years of remaining life, for instance, should appear in the reserves table with a replacement cost estimate in year five, not buried in a narrative paragraph.

Key elements to verify when reviewing any PCA report:

- RUL estimates are system-specific, not building-wide averages that obscure individual component risk

- Cost opinions reflect current local pricing, not national averages that may understate Mid-South labor and material rates

- Deferred maintenance is quantified, not just described, so you can calculate a Facility Condition Index (FCI)

- Report format aligns with lender requirements if financing is involved, since PCA report format and cost tables are as critical as the observations themselves for effective loan structuring

The Facility Condition Index benchmarks building condition by dividing total deferred maintenance costs by the property’s replacement value. An FCI below 0.05 indicates good condition, while anything above 0.10 signals significant capital risk. This single ratio provides portfolio managers with a consistent metric for comparing assets across property types and geographies.

Capital planning negotiations frequently hinge on how the PCA classifies repair timing and RUL assumptions. A seller who disputes an immediate repair classification will often accept a price reduction instead. Knowing which findings are defensible and which are judgment calls gives you leverage at the table.

Common mistakes that undermine a commercial property assessment

The most expensive mistake in any assessment is scope creep in the opposite direction: starting too narrow. Investors who limit their inspection to visible interior conditions and skip the roof, site, or MEP systems routinely discover six-figure deferred-maintenance items after closing. Writing down included and excluded inspection elements before the engagement starts prevents budget overruns and scope disputes.

Other recurring pitfalls include:

- Misreading deferred maintenance as cosmetic: Peeling paint on a parapet wall is not cosmetic. It is a water intrusion warning that may indicate failed flashing below.

- Accepting verbal maintenance histories: Facility managers sometimes overstate the number of completed repairs. Require written service records and cross-reference them against the equipment condition observed on-site.

- Ignoring site improvements: Parking lots, storm drains, and retaining walls carry significant replacement costs that are easy to overlook when attention focuses on the building itself.

- Selecting inspectors on price alone: Inspector qualifications vary widely. ASTM E2018 compliance requires specific professional credentials. An underqualified inspector produces a report that neither lenders nor experienced investors will rely on.

Pro Tip: Request a draft PCA report before the final version is issued. Reviewing the draft allows you to flag missing observations, question RUL assumptions, and confirm that the cost tables align with your lender’s underwriting requirements.

“The most dangerous PCA is the one that looks thorough but omits the systems most likely to fail. A report that covers everything except the 20-year-old chiller is not a risk management tool. It is a liability.”

Many lenders require ASTM-compliant PCAs during acquisition or refinancing transactions to quantify condition risk and inform underwriting. If your report does not meet that standard, you may face delays, additional inspection costs, or revised loan terms at the worst possible moment in a transaction.

Key takeaways

A thorough commercial property condition assessment combines document review, systematic visual inspection, and financial analysis to provide investors with a defensible picture of physical risk and capital exposure.

| Point | Details |

|---|---|

| Start with documents | Maintenance records and construction documents shape RUL estimates before the site visit begins. |

| Follow a structured checklist | Cover all nine system categories to avoid blind spots that translate into unbudgeted capital costs. |

| Read both cost tables | The Immediate Repairs Table and Replacement Reserves Table serve different financial purposes and must not be conflated. |

| Use the FCI benchmark | Divide total deferred maintenance by replacement value to compare condition risk across properties consistently. |

| Define scope in writing | Written scope agreements prevent disputes, missed systems, and cost overruns before the inspection starts. |

Why I think most investors underestimate the PCA process

Most investors treat the PCA as a checkbox. They order it because the lender requires it, skim the executive summary, and move to closing. That approach leaves significant negotiating leverage on the table and, more importantly, it leaves real financial risk unquantified.

What we have seen at Upchurch Inspection is that the investors who get the most value from a PCA are the ones who engage with the process before the inspector ever sets foot on the property. They review the maintenance records themselves. They walk the site with the inspector rather than waiting for the report. They ask why a system received a particular RUL estimate instead of accepting it at face value.

Integrating PCA outcomes into asset management software is the next level of sophistication, and it is more accessible than most owners realize. Platforms that convert PCA cost tables into live capital planning workflows give you a rolling view of your portfolio’s condition risk rather than a static snapshot that ages the moment the report is printed. Thermal imaging and predictive maintenance data can feed into those same systems, turning a one-time assessment into an ongoing management tool.

My honest advice: select your inspection firm based on credentials and report quality, not turnaround time. Review the draft before the final report is issued. And treat the Replacement Reserves Table as a capital budget, not a footnote.

— Holly

How Upchurch Inspection supports your commercial property assessment

Upchurch Inspection delivers ASTM-compliant commercial inspections across the Mid-South, with detailed reports covering structural systems, MEP, roofing, life safety, and site improvements. Our inspectors hold qualifications that exceed state standards, and our reports are structured to meet lender underwriting requirements from day one. Whether you are acquiring a single-tenant retail building or a multi-story office complex, we provide the cost tables, RUL estimates, and deficiency documentation that protect your investment and support your financing. Explore our commercial property inspection guide to understand exactly what a professional PCA covers and how to prepare for one.

FAQ

What is a Property Condition Assessment?

A Property Condition Assessment is a structured evaluation of a commercial building’s physical condition, conducted according to ASTM E2018 standards, that combines document review, a visual walk-through, and cost opinions covering immediate repairs and long-term capital needs.

How long does a commercial property inspection take?

Walk-through time depends on the building’s size and complexity, but most commercial inspections range from two to eight hours on-site, followed by several days of report preparation, including document review and cost analysis.

What is the difference between immediate repairs and replacement reserves?

Immediate repairs are deficiencies requiring attention within 90 days of closing, such as safety hazards or active leaks. Replacement reserves project capital needs over a 12-year horizon for systems approaching the end of their service life.

Do lenders require a PCA before approving a commercial loan?

Most commercial lenders require an ASTM-compliant PCA for acquisition and refinancing transactions because the report quantifies condition risk and informs reserve requirements in the loan structure.

What is the Facility Condition Index and why does it matter?

The Facility Condition Index divides total deferred maintenance costs by the property’s replacement value. A score below 0.05 indicates good condition, while a score above 0.10 signals significant capital risk that should factor into your offer price or lease terms.