TL;DR:

- A property condition assessment (PCA) provides a detailed evaluation of a property’s physical condition to support real estate decisions. Unlike a basic inspection, it estimates costs and useful life of major building systems, complying with ASTM E2018 standards. Buyers, sellers, and lenders use PCA reports to assess risks, plan capital expenses, and avoid unexpected financial losses.

A property condition assessment (PCA) is a structured, formal evaluation of a property’s physical condition that produces a written report used in real estate decision-making. Governed by ASTM E2018 standards, a PCA covers major building systems, site components, and deferred maintenance to give buyers, sellers, lenders, and real estate professionals a clear picture of what they are actually buying or financing. Unlike a basic home inspection, a PCA translates physical observations into capital cost projections and remaining useful life estimates. That distinction matters enormously when money and risk are on the table.

What is a property condition assessment and how does it work?

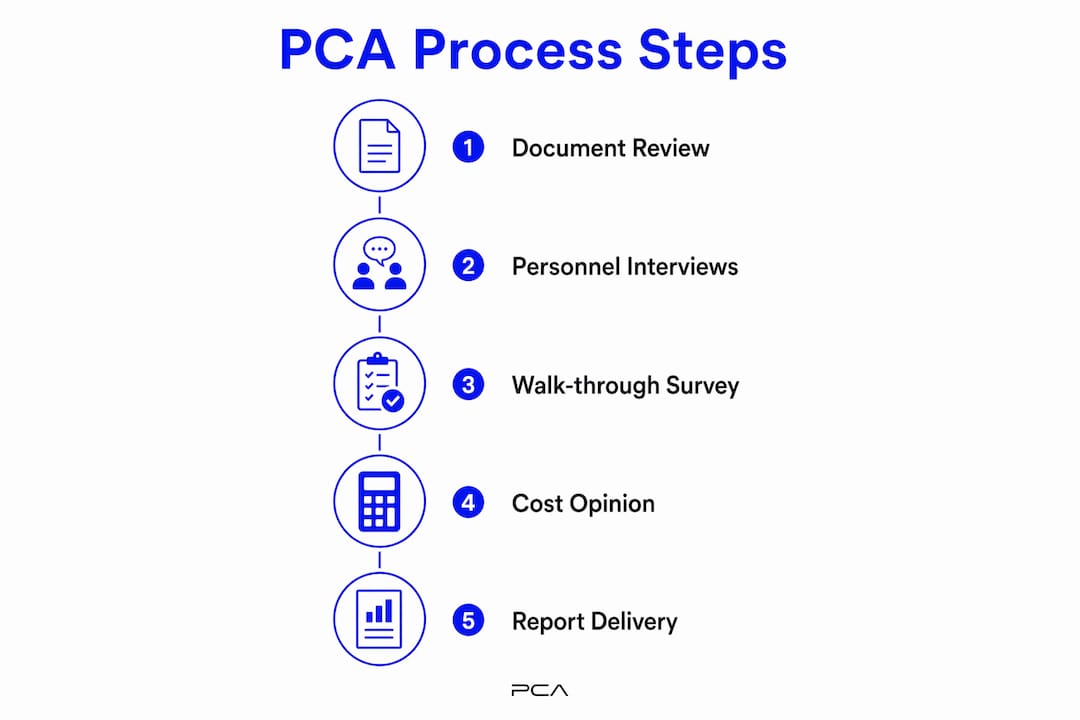

A PCA is a walk-through survey of a property’s physical condition, producing a Property Condition Report (PCR) used in commercial real estate due diligence. The process follows three defined phases: document review, personnel interviews, and a visual walk-through of accessible areas. Each phase feeds the next. Missing any one of them weakens the final report.

The document review phase covers building permits, maintenance records, prior inspection reports, and equipment installation dates. This history is not optional background reading. Skipping the paper review risks flawed remaining useful life assumptions because an assessor cannot accurately estimate when a roof or HVAC system will fail without knowing when it was installed or last serviced.

Personnel interviews follow the document review. The assessor speaks with property managers, maintenance staff, or owners to surface issues that are not visible during a walk-through, such as recurring plumbing backups, past water intrusion events, or deferred repairs. The visual walk-through is non-invasive. Assessors observe and document accessible conditions without opening walls, cutting into systems, or performing destructive testing.

Pro Tip: If a PCA flags a suspected hidden condition, such as concealed moisture damage or foundation movement, the report will recommend a follow-up specialist evaluation. That recommendation is not a failure of the PCA process. It is the process working correctly.

Cost opinions and remaining service life estimates are developed after the walk-through by combining field observations with the document history. The assessor assigns estimated replacement timelines and costs to each major component. That output is what separates a PCA from a standard inspection checklist.

How does a PCA differ from a standard property inspection?

Many buyers and agents use the terms “inspection” and “PCA” interchangeably. That is a common and costly mistake. The two evaluations serve different purposes, follow different standards, and produce different outputs.

| Feature | Standard Home Inspection | Property Condition Assessment |

|---|---|---|

| Governing standard | State licensing requirements | ASTM E2018 |

| Primary output | Defect list | PCR with cost projections and useful life estimates |

| Capital planning data | Rarely included | Core deliverable |

| Typical audience | Residential buyers | Commercial buyers, lenders, investors |

| Report length | 20–50 pages | 50–150+ pages |

| Invasive testing | Sometimes | Never |

A standard home inspection identifies defects at a point in time. A PCA goes further by estimating costs and replacement timing for each major component. That difference is significant for anyone making a capital-intensive purchase or financing decision.

Key distinctions worth knowing:

- A home inspection tells you the roof is aging. A PCA tells you the roof has an estimated five years of remaining useful life and will cost approximately $85,000 to replace.

- A home inspection is typically required by buyers. A PCA is often required by lenders as part of underwriting.

- ASTM E2018 standardization makes PCA results comparable across properties and over time, which matters to institutional investors reviewing multiple assets.

- A PCA report is a formal document suitable for lender submission. A home inspection report is typically written for the buyer’s personal use.

The audience difference drives everything else. Residential buyers need to know what is broken. Commercial buyers and lenders need to know what will cost money and when.

Why are property condition assessments important in real estate transactions?

The main purpose of a PCA is to identify deferred maintenance and potential capital expenses before closing. That information prevents post-sale surprises that can turn a profitable acquisition into a financial problem. Deferred maintenance does not disappear at closing. It transfers to the new owner, often with compounding costs.

For buyers, a PCA provides the data needed to price risk accurately. If the PCR shows $400,000 in capital needs over the next ten years, the buyer can negotiate a price reduction, request seller credits, or walk away with clear justification. Without that data, the buyer is guessing.

For sellers, a PCA completed before listing provides a proactive disclosure tool. Sellers who understand their property’s condition can price it correctly, avoid renegotiation surprises, and demonstrate transparency to buyers. That transparency builds deal confidence and reduces the chance of a transaction falling apart late in the process.

For lenders, the stakes are different but equally serious. Lenders often require PCAs compliant with ASTM E2018 as part of underwriting due diligence to assess collateral condition and capital exposure. A lender financing a $5 million commercial property needs to know whether that asset will require $800,000 in repairs within three years. The PCA answers that question with documented evidence.

A PCA does not just describe what is wrong with a property. It quantifies the financial exposure attached to those conditions, which is the information that actually drives real estate decisions.

Real estate professionals benefit from PCAs as well. Agents and brokers who understand PCA findings can guide their clients through negotiations more effectively, anticipate lender requirements, and reduce the risk of deals collapsing over undisclosed condition issues.

What does a property condition report contain?

A Property Condition Report is the formal written output of a PCA. Its structure follows ASTM E2018 guidance and covers the full scope of the assessment in organized sections. Understanding the report’s structure helps buyers, sellers, and lenders use it correctly rather than just filing it away.

A typical PCR includes these components:

| Report Section | What It Covers |

|---|---|

| Executive summary | High-level findings, total cost estimates, and immediate concerns |

| Site and building systems | Condition of roofing, structure, HVAC, plumbing, electrical, and envelope |

| Deficiency log | Itemized list of observed problems with severity ratings |

| Remaining useful life | Estimated years left for each major component |

| Cost opinions | Estimated repair and replacement costs by component |

| Capital expenditure table | Projected costs organized by immediate, short-term, and long-term horizons |

The PCR summarizes observed deficiencies, remaining service life, and projected maintenance costs, often over a ten-year horizon with an immediate category for urgent needs. That ten-year window is not arbitrary. It aligns with typical commercial loan terms and capital reserve planning cycles.

The immediate category covers repairs needed now or within the next year. Short-term covers years two through five. Long-term covers years six through ten. Clear categorization helps owners and lenders differentiate urgency and plan capital accurately. A buyer reviewing a PCR should focus first on the immediate category and the total ten-year cost projection. Those two numbers define the financial risk of the acquisition.

Pro Tip: Do not read a PCR as a pass/fail document. Every property has deficiencies. The question is whether the cost and timing of those deficiencies are priced into the deal. A PCR gives you the data to answer that question with numbers, not assumptions.

Detailed cost projections over a 10–12 year horizon assist owners in capital reserve planning, which is essential for maintaining property value and meeting lender compliance requirements over the life of a loan.

Key Takeaways

A property condition assessment is the most reliable tool available for quantifying physical risk in a real estate transaction, and skipping one exposes buyers, sellers, and lenders to preventable financial loss.

| Point | Details |

|---|---|

| PCA follows ASTM E2018 | The standard ensures consistent scope, terminology, and cost opinions across all assessments. |

| Three-phase process | Document review, personnel interviews, and visual walk-through together produce accurate findings. |

| PCR covers ten-year costs | The report separates immediate, short-term, and long-term capital needs for clear financial planning. |

| PCA differs from home inspection | A PCA adds remaining useful life estimates and cost projections that a standard inspection does not provide. |

| Lenders require PCAs | ASTM E2018-compliant reports are a standard underwriting requirement for commercial real estate financing. |

Why I think most buyers misread a PCA report

Most buyers receive a PCR and immediately search for the biggest dollar number in the document. That instinct is understandable, but it misses the point. The number that matters most is not the single largest line item. It is the total immediate cost combined with the five-year capital projection. Those two figures tell you what you will actually spend in the near term, not what might happen in year nine.

The second mistake I see regularly is treating a PCA as a negotiation weapon rather than a planning document. A PCR showing $200,000 in deferred maintenance does not automatically mean you demand a $200,000 price reduction. It means you now understand the property’s true cost of ownership. Some of those costs are already priced into the asking price. Others are not. A good assessor can help you tell the difference.

The third issue is confusing a PCA with a specialized inspection. A PCA is non-invasive and does not include environmental testing, structural engineering analysis, or code compliance reviews. If the assessor flags a suspected structural concern, that flag is a referral, not a conclusion. Follow it up with the right specialist before closing.

The buyers and sellers who get the most value from a PCA are the ones who read the full report, ask the assessor to walk them through the findings, and use the capital expenditure table to build a realistic post-closing budget. That is the real estate condition evaluation process working as it should.

— Holly

How Upchurchinspection supports your real estate decisions

Upchurchinspection provides property condition assessments for commercial and residential properties across the Mid-South, with inspectors whose qualifications exceed state standards. The reports cover major systems including plumbing, electrical, HVAC, and structural components, and are written to give buyers, sellers, and lenders the specific data they need to make informed decisions. For property owners who want to stay ahead of capital costs, the benefits of regular inspections extend well beyond any single transaction. Upchurchinspection also offers commercial real estate due diligence inspections for buyers and lenders who need ASTM-aligned documentation before closing.

FAQ

What is the ASTM E2018 standard for PCAs?

ASTM E2018 is the industry standard that defines the scope, process, and reporting requirements for property condition assessments. It covers document review, interviews, visual inspection, and cost opinions to ensure consistent, comparable results across properties.

How long does a property condition assessment take?

The walk-through portion of a PCA typically takes several hours for a mid-size commercial property. The full process, including document review, interviews, and report preparation, generally takes one to two weeks depending on property size and complexity.

Who pays for a property condition assessment?

The buyer or borrower typically pays for a PCA as part of due diligence costs. In some transactions, lenders order the PCA directly and pass the cost to the borrower as part of the loan origination process.

Can a PCA replace a home inspection for residential buyers?

A PCA is not a substitute for a standard home inspection in a residential transaction. Home inspections address consumer-focused safety and defect disclosure requirements, while a PCA is designed for capital planning and lender due diligence in commercial contexts.

What happens if a PCA finds serious deficiencies?

Serious deficiencies identified in a PCR give buyers grounds to renegotiate price, request seller remediation, or exit the contract during the due diligence period. Lenders may also require repairs or reserve escrows before approving financing.