A commercial roof does not have to be actively leaking to be a serious financial risk.

That is one of the most important things buyers, investors, trustees, lenders, and property owners need to understand before closing on a commercial building.

During a walkthrough, the roof is often out of sight. The buyer may spend time looking at tenant spaces, offices, classrooms, warehouse areas, restrooms, parking lots, and mechanical rooms. The broker may say the roof is fine. The seller may say there have not been any major leaks. The building may even look dry inside on the day of the showing.

But “not leaking today” is not the same thing as “low risk.”

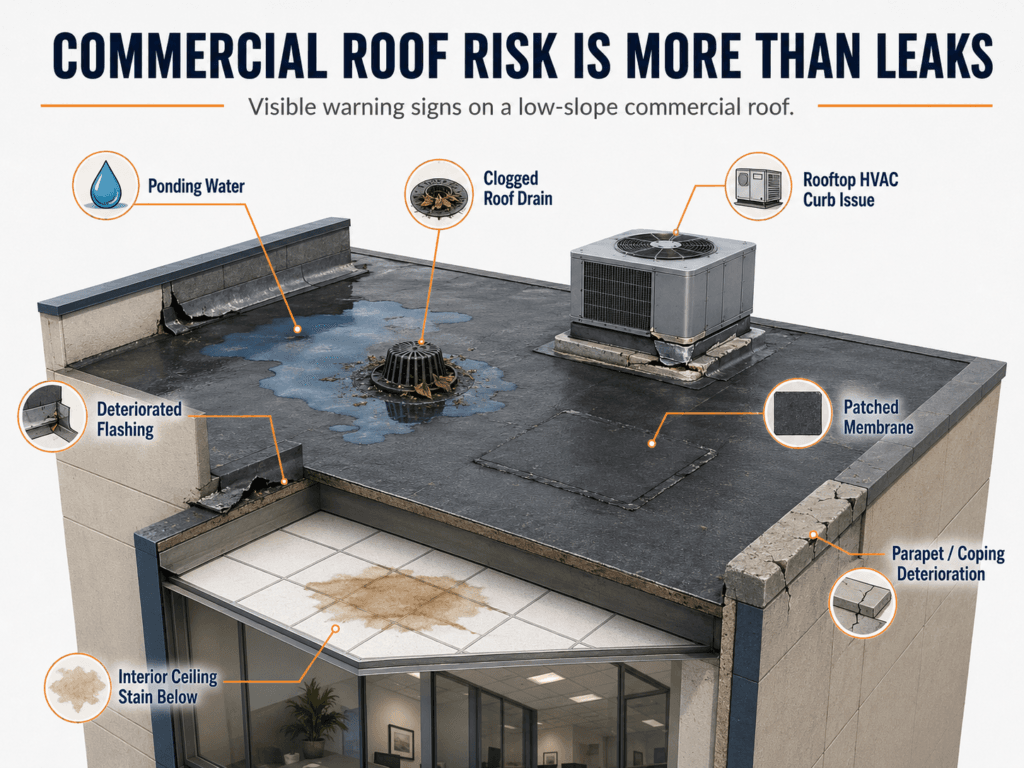

Commercial roofs age slowly, and many of the warning signs appear long before water is dripping into the building. Ponding water, clogged drains, deteriorated flashing, open seams, patched membrane, damaged coping, soft areas, roof-mounted HVAC curb issues, and poor drainage can all point to future expense.

For a commercial buyer, the roof is not just a building component.

It is a capital risk.

At Upchurch Inspection, we look at commercial roofs as part of the larger due diligence picture. The question is not simply whether the roof is leaking at the moment. The better question is whether the roof system, drainage, visible condition, and maintenance history suggest that the buyer may be inheriting a major repair or replacement obligation.

Commercial Roofs Are Different From Residential Roofs

A residential roof is usually visible from the ground. It may be steep enough to shed water quickly. A homebuyer can often see missing shingles, obvious wear, damaged gutters, or flashing concerns without much difficulty.

Commercial roofs are different.

Many commercial buildings have low-slope or flat roof systems. These roofs do not shed water the same way a steep residential roof does. Instead, they rely heavily on proper drainage, membrane condition, seams, flashing, penetrations, and maintenance.

That changes the inspection.

A low-slope commercial roof may have internal drains, scuppers, gutters, parapet walls, expansion joints, roof-mounted equipment, service walkways, patched areas, membrane seams, and multiple penetrations. The system may also include insulation, tapered drainage components, coatings, and different roof sections from different eras.

A buyer standing in the parking lot may see almost none of that.

That is why roof access and roof-level evaluation matter when conditions allow. A roof that looks acceptable from below may tell a different story once the surface, drainage paths, penetrations, and equipment curbs are reviewed more closely.

The Real Question Is Roof Risk

Commercial buyers often ask, “Does the roof leak?”

That is a fair question, but it is not enough.

A better set of questions would be:

How old is the roof? What type of roof system is installed? Has it been repaired repeatedly? Are drains functioning? Is water ponding? Are seams opening? Are flashings deteriorated? Are rooftop HVAC units creating roof penetrations or curb concerns? Are there interior stains that suggest prior leaks? Are maintenance records available? Is there a warranty? Has a roofing contractor recently evaluated the roof?

Those questions give a much clearer picture of risk.

A roof can be patched and functional while still being near the end of its useful life. A roof can be dry on inspection day while showing drainage problems that accelerate deterioration. A roof can have no active leak during a walkthrough but still require major work within a few years.

For a commercial buyer, that matters because roof work can be expensive, disruptive, and difficult to ignore once the property is owned.

The roof is one of those systems where a small misunderstanding before closing can become a major financial problem after closing.

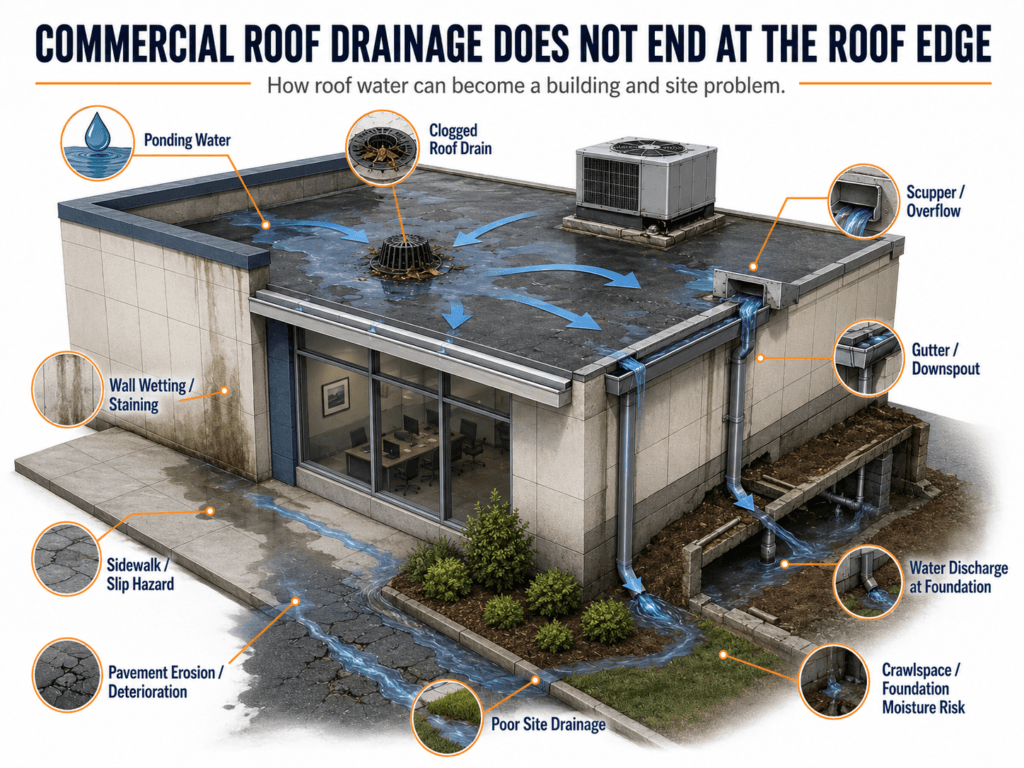

Drainage Is the Heart of Commercial Roof Performance

Water management is one of the biggest issues with commercial roofs.

A low-slope roof is not designed to hold water indefinitely. It may have a slight slope that directs water toward drains, scuppers, gutters, or downspouts. When that drainage system works properly, water leaves the roof in a controlled way. When it does not, water begins to sit, spread, and find weaknesses.

Ponding water is one of the most important conditions to watch for.

Water that remains on the roof after rainfall can accelerate membrane deterioration, stress seams, collect debris, encourage biological growth, add load, conceal damage, and increase the chance of leaks. It can also indicate settlement, poor slope, clogged drains, inadequate design, or previous repair work that changed the roof surface.

In the Mid-South, roof drainage deserves special attention because heavy rain is common, humidity is high, and buildings often experience repeated wetting and drying cycles. A roof that does not drain well may age faster than expected.

Drainage issues are also not limited to the roof surface. Water has to go somewhere after it leaves the roof. If gutters overflow, downspouts discharge at the foundation, scuppers dump water onto walls, or roof drains discharge into questionable piping, the problem may move from the roof to the building exterior, foundation, pavement, crawlspace, or interior.

A commercial roof inspection should not just ask whether water leaves the roof.

It should ask whether water leaves the property in a way that protects the building.

Ponding Water Is Not Just a Cosmetic Issue

Ponding water is easy to underestimate.

To some buyers, it may look like a little standing water on a flat roof. But to an inspector, it can be one of the strongest signs that the roof system deserves closer attention.

Ponding water can shorten roof life. It can create more severe wear in specific areas. It can collect leaves, dirt, and debris that block drains. It can make maintenance harder. It can hide cracks, punctures, seams, or deteriorated membrane. In colder conditions, standing water can also contribute to expansion and contraction issues.

More importantly, ponding tells a story.

It may suggest that the roof was not properly sloped, that insulation has compressed, that the structure has settled, that drainage components are clogged, or that prior roof work was poorly executed.

A buyer does not need to know every technical cause during the initial inspection. But the buyer does need to know that ponding water is a meaningful risk indicator.

If ponding is observed, a commercial roofing contractor may need to evaluate the roof before closing, especially if the roof is aged, patched, soft, stained, or has interior leak evidence below.

Flashing Is Where Many Roof Problems Begin

Roofs rarely fail only in the middle of an open field of membrane.

Many failures begin at transitions.

Flashing exists where the roof meets something else: walls, parapets, curbs, skylights, vents, pipes, drains, scuppers, equipment supports, edges, and penetrations. These areas are naturally more vulnerable because materials change direction, move differently, or depend on sealants and workmanship.

On commercial roofs, flashing concerns may appear around parapet walls, roof edges, mechanical curbs, pipe penetrations, rooftop unit platforms, drains, and wall intersections.

Deteriorated flashing may not create an active leak immediately. But it creates an opening in the roof’s defense system. Sealants crack. Metal corrodes. Membranes pull away. Fasteners loosen. Old repairs fail. Water finds the weakest point.

A buyer should pay close attention to flashing because it often reveals the quality of maintenance.

A roof with clean, well-maintained flashing details tells one story. A roof with cracked sealant, exposed fasteners, patch material, open gaps, and deteriorated transitions tells another.

Rooftop HVAC Units Create Roof Risk Too

Commercial roofs and HVAC systems are closely connected.

Many commercial buildings have rooftop units, and every rooftop unit introduces roof-related concerns. The unit sits on a curb or support system. Refrigerant lines, electrical conduit, gas piping, ductwork, and condensate lines may all interact with the roof. Technicians may walk across the roof to service the equipment. Panels may be removed, tools may be dropped, and repairs may be performed over time.

That means the area around rooftop HVAC units deserves careful review.

Common concerns include deteriorated curb flashing, rusted equipment, poor sealant, damaged membrane from service traffic, ponding water near units, condensate discharge onto the roof surface, unsupported lines, roof patches around equipment, and evidence of leaks below.

This is where mechanical risk and roof risk overlap.

A buyer may think of RTUs as an HVAC issue, but they can also affect the roof. A poorly flashed curb can leak. A condensate line can discharge water onto the membrane. Repeated service traffic can damage the roof. Rusted equipment can stain and deteriorate surrounding areas. Old equipment replacement may disturb roof details.

When a commercial building has several rooftop units, those concerns multiply.

The roof inspection should not ignore mechanical equipment just because the HVAC system itself may require a separate specialist. The roof still has to manage all those penetrations, curbs, and service impacts.

Prior Repairs Can Be Helpful or Concerning

A patched roof is not automatically a bad roof.

Roofs require maintenance. Repairs are expected over time. A well-documented repair made by a qualified roofing contractor may show responsible ownership.

But repeated patching, inconsistent materials, amateur repairs, heavy sealant use, and repairs without documentation can raise concern.

A roof with scattered patches may be telling the buyer that leaks have occurred before. The important question is whether those repairs addressed isolated conditions or whether they are signs of a roof system that has been failing in stages.

Interior conditions can help add context. If patched roof areas align with stained ceiling tiles, damaged drywall, wet insulation, or tenant complaints, the roof history becomes more important.

A buyer should ask for repair records, warranty information, and leak history. If the seller cannot provide documentation, the buyer may need to treat the roof with more caution.

The absence of documentation does not prove the roof is defective.

But it does increase uncertainty.

And uncertainty in commercial due diligence usually means risk.

Interior Stains May Be the Roof Telling on Itself

Commercial roof problems often show up inside before anyone fully understands the roof condition.

Stained ceiling tiles, damaged drywall, peeling paint, water marks, musty odors, rusted ceiling grid, damaged insulation, and repairs below roof areas can all suggest previous or ongoing water intrusion.

These signs should not be dismissed just because the interior is dry during the inspection.

Leaks are not always active at the moment they are observed. Some occur only during wind-driven rain. Some occur only when drains are clogged. Some occur only during heavy storms. Some appear after water travels along framing, ductwork, or ceiling systems before showing up far from the actual roof entry point.

A stained ceiling tile is not a roof diagnosis by itself.

But it is evidence.

When interior staining appears below an aged, patched, ponding, or poorly drained roof, the buyer should slow down and take the condition seriously.

Parapet Walls and Roof Edges Deserve Attention

Commercial roof edges are another common risk area.

Many low-slope roofs terminate at parapet walls, coping caps, metal edges, gutters, or scuppers. These details are exposed to weather, movement, wind, and maintenance conditions. When they deteriorate, water can enter behind the roof covering or wall assembly.

Parapet walls can be especially important because they are both wall and roof-related components. Deteriorated masonry, cracked coping, failed sealant, open joints, poor flashing, and loose metal caps can all create water entry points.

A roof edge problem may not show up as an obvious leak right away. Water may enter the wall, affect masonry, damage interior finishes, or contribute to hidden deterioration over time.

Buyers often focus on the broad roof surface, but edges and parapets may tell just as much about the roof’s risk level.

Roof Access and Inspection Limitations Matter

Not every commercial roof can be safely accessed during an inspection.

Access may be limited by height, weather, lack of ladders, unsafe roof surfaces, steep sections, fragile materials, tenant restrictions, locked access points, or other safety concerns. In some cases, drone photography or ground-level observations may help, but they are not the same as full roof access.

Limitations matter.

If the roof is not accessed, the report should say so clearly. If only part of the roof is visible, that should be stated. If stored materials, equipment, weather, or unsafe conditions limit evaluation, the buyer needs to know.

A roof that cannot be fully evaluated is not automatically bad.

But the buyer should understand that risk remains unresolved.

For a major commercial purchase, unresolved roof risk may justify further evaluation by a commercial roofing contractor before the due diligence period ends.

This is especially true when roof replacement would be a major capital expense.

Roof Documentation Should Be Requested

A visual inspection is important, but documentation can change the picture.

Commercial buyers should request roof-related records whenever possible. Useful documents may include installation records, warranty information, roof plans, repair invoices, maintenance logs, leak history, contractor reports, insurance claim records, coating records, and prior inspection reports.

Documentation helps answer questions that may not be fully visible during the inspection.

When was the roof installed? What system is it? Who installed it? Is there a warranty? Is the warranty transferable? Have repairs been made? Were repairs made by a qualified contractor? Have there been recurring leaks? Have drains been maintained? Has the roof been coated? Were roof-mounted units added later?

A seller with organized roof records gives the buyer more to work with.

A seller who cannot answer basic roof questions leaves the buyer with uncertainty.

Again, uncertainty is not proof of failure. But it should influence how the buyer evaluates risk.

Commercial Roof Risk Can Affect Negotiation

A roof concern does not automatically kill a deal.

Many commercial properties have roof issues. Some are manageable. Some are already priced into the deal. Some can be repaired. Some require replacement. Some require a specialist’s opinion before the buyer can make a responsible decision.

The point is not to panic.

The point is to quantify the risk as much as possible before closing.

Roof findings may lead the buyer to request contractor evaluation, obtain repair or replacement estimates, negotiate a credit, request seller repairs, extend the due diligence period, adjust capital reserves, or reconsider the purchase price.

A buyer may still move forward after discovering roof concerns. But they should move forward with clear eyes.

There is a major difference between knowingly buying a building with a roof nearing replacement and discovering that fact six months after closing.

Roof Drainage Connects to Site Drainage

Commercial roof drainage does not stop at the roof edge.

Once water leaves the roof, it must be carried away from the building. If roof water discharges at the foundation, dumps onto sidewalks, overwhelms gutters, floods landscaping, erodes soil, or contributes to pavement damage, the roof drainage problem becomes a site drainage problem.

This is common in many properties.

A roof may have gutters and downspouts, but the downspouts may terminate too close to the building. Scuppers may dump water onto lower roof sections or wall surfaces. Internal drains may discharge into systems that are not visible or not verified. Roof water may flow across walkways, creating slip hazards. Large roof areas may overload poorly designed drainage paths.

In the Mid-South, where heavy rain is common, this matters.

A commercial building needs a complete water management strategy. Roof water should be collected, controlled, and discharged in a way that protects the structure and site.

If roof drainage is poor, the buyer may inherit more than a roof issue. They may inherit foundation concerns, pavement deterioration, exterior wall damage, crawlspace moisture, erosion, or tenant complaints.

Water problems rarely stay in one category.

A Roof That Looks Serviceable May Still Need Specialist Review

Commercial inspections and Property Condition Assessments can identify visible roof concerns and recommend further evaluation, but they do not replace a full roof certification, design review, moisture scan, core sampling, warranty review, or contractor estimate unless those services are specifically included.

That is why specialist follow-up is sometimes necessary.

A commercial roofing contractor may be needed when the roof is aged, patched, ponding, damaged, inaccessible, undocumented, actively leaking, or potentially near replacement. A contractor can often provide repair options, replacement estimates, warranty information, and a more detailed roof-specific opinion.

For larger assets, that extra step can be critical.

The buyer does not need to guess. If the roof may affect the deal, get more information before closing.

A commercial roof can be dry on inspection day and still be a major financial risk. The real question is not only whether it leaks today, but how much roof and drainage risk the buyer is inheriting.

-Wes Upchurch, Upchurch Inspection

The Report Should Explain Why the Roof Matters

A good commercial inspection report should not simply say, “Roof has ponding water” or “Flashing is deteriorated.”

It should explain why the condition matters.

Commercial buyers, lenders, trustees, investors, and boards need context. They need to know whether a condition appears minor, maintenance-related, potentially costly, urgent, or in need of specialist review. They need to know what limitations applied and whether documentation was available.

A useful roof section should help the client understand the relationship between visible conditions and ownership risk.

For example, ponding water on an aged low-slope roof with prior patching may be more significant than isolated debris in a gutter. Deteriorated flashing around several rooftop units may be more concerning than one small sealant gap. Interior staining below a patched roof area may carry more weight than staining with a clearly documented and repaired source.

The report should help the buyer think, not just react.

Final Thoughts

Commercial roof inspections are not just about finding leaks.

They are about understanding roof risk.

A commercial roof can be dry on inspection day and still carry significant concerns. Poor drainage, ponding water, deteriorated flashing, roof-mounted equipment issues, prior patching, membrane wear, clogged drains, parapet deterioration, and interior staining can all point to future cost.

For buyers, investors, trustees, lenders, and property owners, the roof deserves serious attention because it can become one of the largest capital expenses on the property.

The right question is not only whether the roof leaks today.

The better question is:

What roof and drainage risk is the buyer inheriting?

That is the question a commercial inspection or Property Condition Assessment should help answer.

Because after closing, the roof is no longer the seller’s problem.

It becomes part of the buyer’s financial reality.

Need a Commercial Roof or Property Inspection?

Upchurch Inspection provides commercial property inspections and Property Condition Assessments for buyers, investors, trustees, lenders, property owners, and real estate professionals throughout the Mid-South.

We evaluate commercial buildings with attention to visible roof condition, drainage concerns, roof-mounted equipment, deferred maintenance, major system risks, and practical decision-making before closing or major investment.

For commercial buildings, churches, campuses, warehouses, multifamily properties, retail spaces, offices, and mixed-use properties, we can help determine the right inspection scope for the decision being made.

To discuss a commercial property inspection or roof-focused assessment, contact Upchurch Inspection.