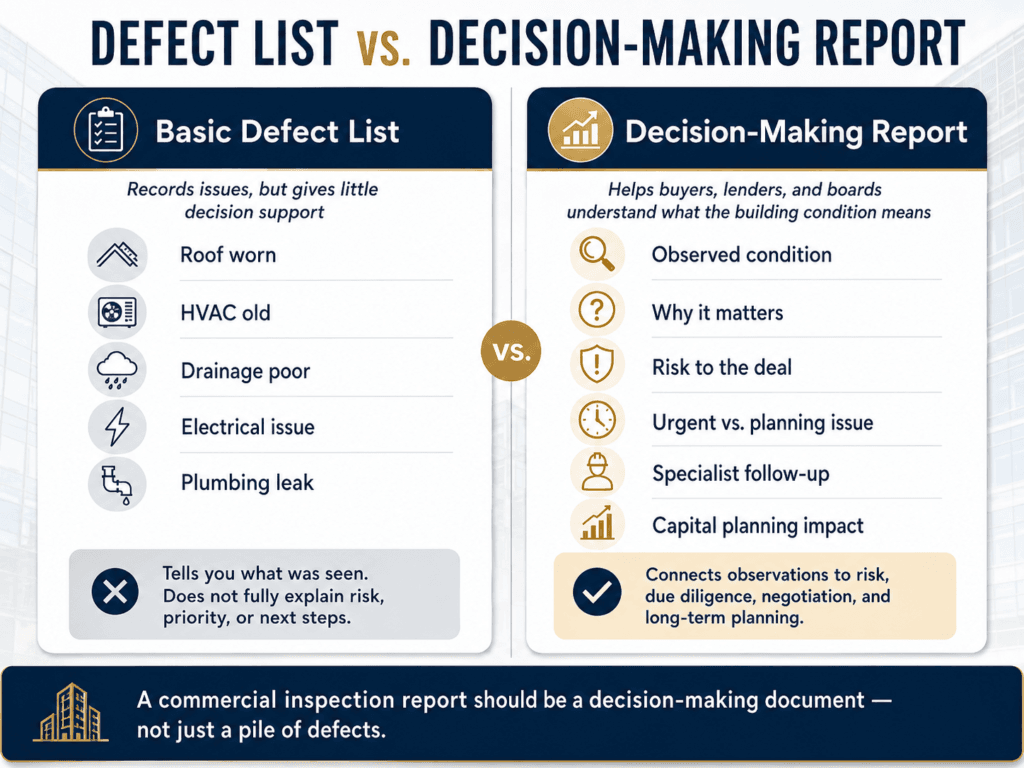

A commercial inspection report should not be a pile of defects.

It should be a decision-making document.

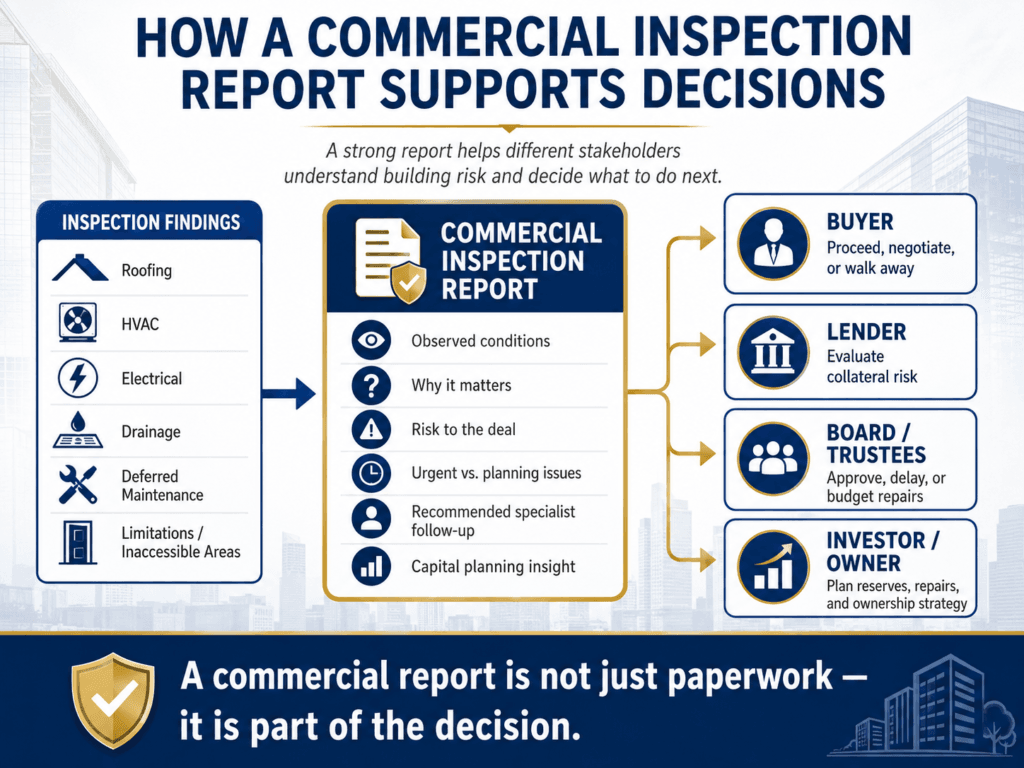

That matters because commercial property decisions are rarely made by one person alone. A residential buyer may read an inspection report at the kitchen table with their agent. A commercial report may be reviewed by buyers, investors, lenders, trustees, board members, attorneys, brokers, property managers, facility directors, insurance representatives, and contractors.

Many of those people were not present during the inspection.

They did not walk the roof. They did not stand in the mechanical room. They did not see the drainage problem at the rear wall. They did not look at the aging rooftop units, the stained ceiling tiles, the cracked pavement, the patched plumbing, or the electrical conditions in the service area.

That means the report has to stand on its own.

A good commercial inspection report should explain what was observed, why it matters, what limitations existed, what risks may require further evaluation, and how the findings may affect the buyer’s decision before closing or major investment.

At Upchurch Inspection, we believe a commercial report should do more than document defects. It should help the client understand the physical condition of the property in a way that supports risk management, negotiation, capital planning, and responsible decision-making.

A Commercial Report Has a Different Job Than a Residential Report

A residential inspection report is usually written for a homebuyer trying to understand the condition of a house. The report may help with repair requests, maintenance planning, and general peace of mind.

A commercial report has a broader job.

It may need to support a purchase decision, lender review, board discussion, investor approval, capital reserve planning, repair negotiation, insurance conversation, or post-closing maintenance strategy.

That changes the writing.

A commercial report cannot simply say, “HVAC is old,” and move on. If several rooftop units are aged, visibly deteriorated, undocumented, and possibly near the end of useful service, that condition may affect capital reserves, tenant comfort, operations, and negotiation strategy.

The report should explain that.

A commercial report cannot simply say, “Roof has ponding water,” without context. The reader needs to understand that ponding water on a low-slope roof may accelerate deterioration, indicate drainage problems, and justify further evaluation by a commercial roofing contractor.

The report should connect the observation to the risk.

That is the difference between a defect list and a useful commercial assessment.

The Report Should Answer the Client’s Real Question

The client is not only asking, “What is wrong with the building?”

The real question is usually deeper.

A buyer may be asking whether the property still makes financial sense. A lender may be asking whether physical conditions could affect collateral risk. A church board may be asking whether the campus will require major repairs after purchase. An investor may be asking whether deferred maintenance will affect cash flow. A property owner may be asking how to prioritize repairs over the next few years.

A good report should help answer those questions.

It should not overpromise. A commercial inspection is not a guarantee, engineering study, environmental assessment, code compliance audit, or contractor bid unless those services are specifically included. But within the agreed scope, the report should provide useful context.

If the roof appears aged and patched, the report should say more than “roof worn.” If multiple plumbing concerns appear across a multifamily property, the report should explain whether the pattern suggests possible systemic maintenance issues. If electrical modifications appear amateur, the report should identify the concern and recommend appropriate evaluation. If a parking lot is deteriorated and holding water, the report should connect that condition to repair planning and site drainage risk.

The report should help the client think clearly.

Major System Summaries Matter

Commercial properties can be complex.

A report that only lists individual observations can make it hard for decision-makers to understand the overall condition of the asset. That is why major system summaries are important.

A useful commercial report should help the reader understand the general condition of major systems such as roofing, exterior envelope, structure, site drainage, parking areas, HVAC, electrical, plumbing, interior areas, and life-safety-related observations within the inspection scope.

These summaries should not replace detailed findings. They should frame them.

For example, the roof section should help the reader understand whether roof concerns appear minor, maintenance-related, aged, undocumented, active, or potentially capital-intensive. The HVAC section should explain whether equipment appears generally serviceable, aging, poorly maintained, inconsistent, or in need of specialist review. The site section should help the reader understand whether drainage and pavement conditions are routine or may affect cost, safety, or long-term performance.

Decision-makers need the forest and the trees.

A board member or lender may not read every individual note with the same attention as the buyer. But they need a clear picture of the major risks. Strong summaries help them see what matters.

Photos Should Explain, Not Just Prove

Commercial reports should include photos, but photos alone are not enough.

A photo should support the explanation. It should help the reader understand the condition, location, severity, or pattern. A close-up photo of a roof patch may be useful, but it becomes more useful when the report explains that the patching was observed in multiple areas of an aged low-slope roof with interior staining below.

A picture of a rusted rooftop unit is helpful, but the report should explain why it matters: the unit appears aged, service records were not provided, visible deterioration was present, and further evaluation may be appropriate before closing.

A photo of ponding water, cracked pavement, stained ceiling tiles, damaged electrical components, or plumbing leaks should not sit in the report like a disconnected image.

The reader should not have to guess why the photo matters.

Good reporting uses photos as evidence, but the narrative gives the evidence meaning.

Limitations Should Be Clear and Practical

Every inspection has limitations.

Commercial inspections often have more limitations than residential inspections because the properties are larger, more complex, and often occupied or partially inaccessible.

The roof may not be safely accessible. Tenant spaces may be locked. Electrical panels may be blocked. Mechanical equipment may be shut down. Stored materials may conceal walls and floors. Weather may limit evaluation. Utilities may be off. Documentation may not be provided. Specialized systems may be outside the agreed scope.

These limitations should be clearly stated.

But limitations should not be buried as generic disclaimers that nobody reads. They should be practical and tied to risk.

If the roof was not accessed, the client needs to know that unresolved roof risk remains. If several tenant spaces were inaccessible, the client should understand that conditions in those spaces were not verified. If maintenance records were not provided, the client should understand that system age, repair history, and service quality may be uncertain.

Limitations are not just legal language.

They are part of the due diligence picture.

A useful commercial report tells the client not only what was observed, but also what could not be confirmed.

The Report Should Identify Deferred Maintenance Patterns

Deferred maintenance is one of the most important stories a commercial report can tell.

Many commercial buildings are not failing dramatically. They are aging unevenly because maintenance has been delayed, minimized, or handled reactively.

That pattern may show up in small ways across the property. Roof sealants are failing. HVAC units are dirty or rusted. Gutters are clogged. Ceiling tiles are stained. Parking lot cracks are spreading. Exterior paint and sealant are deteriorated. Plumbing repairs appear patchy. Electrical labels are missing. Doors do not close properly. Drainage is poor. Mechanical rooms are neglected.

One item may be minor.

A repeated pattern may be meaningful.

A strong report should identify when multiple observations point to deferred maintenance. That helps the client understand whether the building has been managed proactively or whether the buyer may inherit years of delayed work.

Commercial clients need that context because deferred maintenance affects money.

It affects capital reserves, repair priorities, tenant satisfaction, lender confidence, negotiation leverage, and long-term ownership planning.

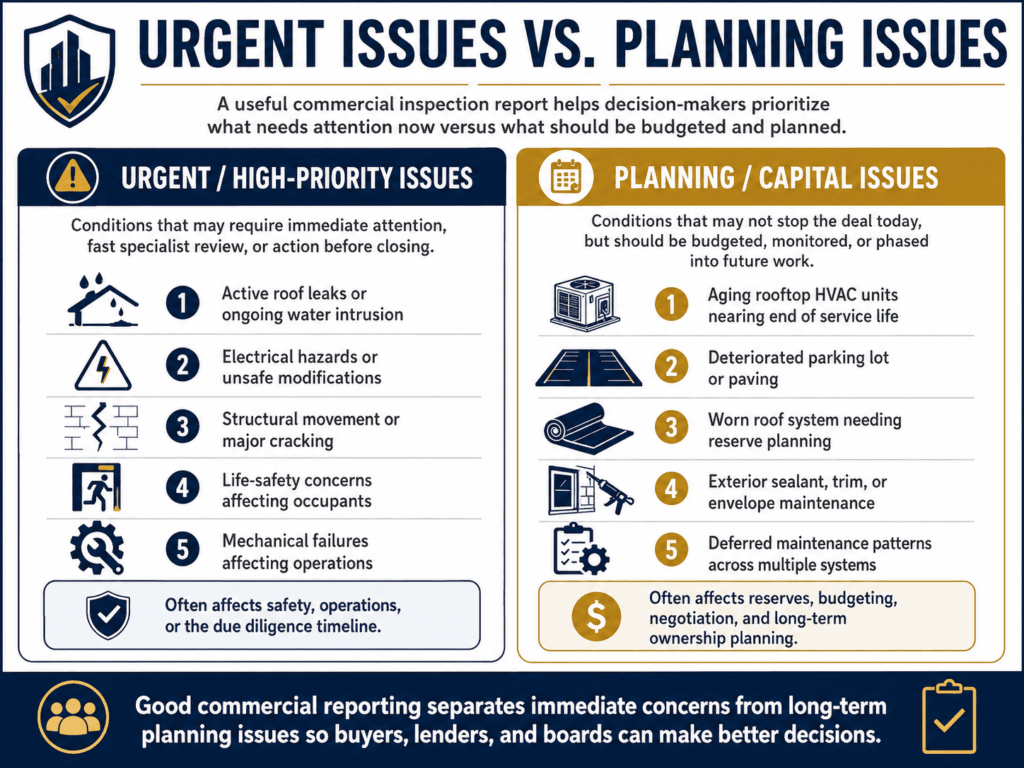

The Report Should Separate Urgent Issues From Planning Issues

Not every defect deserves the same reaction.

Some findings may require immediate attention because they involve safety, active leakage, electrical hazards, water intrusion, structural movement, or conditions that could worsen quickly. Other findings may be routine maintenance. Others may be capital planning concerns that do not require immediate repair but should be budgeted.

A report that treats every item the same does not help the client prioritize.

For commercial buyers, prioritization matters because the cost of correcting everything at once may be unrealistic. A buyer, board, or property owner may need to decide what must be addressed before closing, what should be negotiated, what requires specialist evaluation, what can be phased after closing, and what belongs in a long-term maintenance plan.

A useful report helps organize that thinking.

For example, an unsafe electrical condition may be an immediate concern. An aged roof may require specialist evaluation and capital planning. Minor sealant deterioration may be a maintenance item. Several older RTUs may not be failing today but may require replacement reserves. Deteriorated pavement may need repair planning but may not stop the transaction.

That distinction is the difference between information and noise.

Specialist Recommendations Should Be Specific

Commercial buildings often require specialist follow-up.

That may include a commercial roofing contractor, HVAC contractor, electrician, plumber, structural engineer, sewer camera provider, environmental consultant, fire protection contractor, elevator contractor, accessibility specialist, or other qualified professional depending on the property.

A good report should not vaguely say, “Have this checked.”

It should explain why specialist evaluation is recommended and why timing matters.

If the finding may affect the purchase decision, the report should make that clear. For example, roof concerns should be evaluated before the end of the due diligence period if the roof condition may affect negotiation or capital reserves. HVAC concerns should be reviewed before closing if multiple units appear aged or in questionable condition. Structural movement should be evaluated before the buyer accepts the property’s risk.

Specialist recommendations are not just repair advice.

They are due diligence instructions.

The report should help the client know what to do next.

A Commercial Report Should Support Negotiation

A commercial inspection report often becomes part of the negotiation process.

That does not mean the inspector is negotiating for the client. It means the report provides documentation the client can use to make requests, ask for credits, seek repairs, extend due diligence, obtain estimates, or reconsider the terms of the deal.

For that reason, vague reporting weakens the client.

A statement like “roof needs work” is less useful than a clear description of visible roof conditions, roof access limitations, interior staining, drainage concerns, and the recommendation for commercial roofing contractor evaluation.

A statement like “HVAC old” is less useful than explaining that multiple rooftop units appear aged, several show visible deterioration, service records were not provided, and replacement planning may be needed.

Better documentation creates better leverage.

The report does not have to exaggerate. In fact, it should not. It should be grounded, factual, and clear.

Commercial clients do not need drama.

They need documentation.

Lenders Need to Understand Collateral Risk

When lenders are involved, physical condition can matter.

A lender may not care about every small defect, but major roof issues, structural concerns, deferred maintenance, environmental concerns, safety issues, or large near-term capital needs can affect the risk profile of the property.

A commercial inspection report or Property Condition Assessment can help provide a clearer picture of those physical risks.

This is especially important when the property is older, complex, income-producing, or tied to a larger loan decision. A building with major deferred maintenance may still be financeable, but the lender and borrower need to understand what physical issues may affect the asset.

A report that clearly identifies major systems, limitations, and recommended follow-up is more useful than one that simply lists defects without context.

The lender may not need every detail.

But they do need to understand the major concerns that could affect the property’s performance or value.

Boards and Trustees Need Clear, Defensible Information

Churches, schools, nonprofits, and institutional buyers often need reports that can be reviewed by a board.

That board may include people with different backgrounds. Some may understand construction. Others may not. Some may focus on finances. Others may focus on operations, ministry, safety, or long-term planning.

A useful report should be understandable to all of them.

It should explain major conditions without talking down to the reader. It should be detailed enough to support responsible decision-making, but clear enough that non-technical stakeholders can understand the risk.

For a church or nonprofit board, the report may influence whether to buy a campus, approve a renovation, raise funds, negotiate repairs, seek financing, or delay a decision.

That is serious.

A board does not need a report that simply says “defective” fifty times. It needs a document that helps responsible people understand what the building may require.

Investors Need the Report to Connect to Money

Investors read commercial reports differently.

They want to know how the building condition may affect the deal.

That includes operating expenses, capital expenses, tenant satisfaction, rent assumptions, repair credits, reserve planning, insurance concerns, and post-closing maintenance.

A report that identifies physical defects without connecting them to ownership risk may not be enough.

If the property has repeated plumbing problems, the investor needs to know whether that may suggest a systemic issue. If multiple HVAC systems are aging, the investor needs to understand possible replacement cycles. If the parking lot is deteriorated, the investor needs to consider repair costs and tenant impact. If roof drainage is poor, the investor needs to consider water intrusion and future roof expenses.

Commercial inspection reporting should help investors test the assumptions behind the deal.

The report will not build the financial model for them. But it should give them physical condition information that informs the model.

The Executive Summary Should Not Replace the Full Report

Executive summaries can be useful, especially for commercial clients.

A summary can highlight major concerns, urgent issues, safety-related observations, capital risk areas, scope limitations, and recommended specialist evaluations. For busy buyers, lenders, and boards, this can help focus attention quickly.

But an executive summary should not replace the full report.

The full report contains the detail, context, photos, limitations, and supporting observations that explain the summary. Decision-makers should use the summary as a guide, not as the entire due diligence record.

A strong report gives both: a clear summary of major concerns and detailed sections that support the conclusions.

That balance matters.

Too much detail without summary can overwhelm the client. Too much summary without detail can weaken the documentation.

The Report Should Be Honest About Scope

Commercial inspection scope can vary widely.

A small commercial inspection is not the same as a full ASTM-style Property Condition Assessment. A limited-scope walkthrough is not the same as a specialist-coordinated assessment. A general building inspection is not the same as a roof certification, environmental assessment, structural engineering report, fire inspection, ADA compliance audit, or code compliance review.

The report should make the scope clear.

Clients should know what was included, what was excluded, what was limited, and what additional evaluations may be appropriate.

This protects the client as much as the inspector.

A buyer who understands the scope can make better decisions. If environmental due diligence was not included, they know to obtain it separately. If elevators were excluded, they can bring in an elevator contractor. If the roof was inaccessible, they can request access or specialist review. If cost opinions were not part of the scope, they can obtain contractor pricing.

Scope clarity prevents false confidence.

And false confidence is dangerous in commercial real estate.

A commercial inspection report should not just tell the client what is wrong. It should help decision-makers understand what the property’s condition means for the deal.

-Wesley Upchurch, Upchurch Inspection

The Report Should Be Written in Plain Language

Commercial inspection reporting should be professional, but it should not be unreadable.

Technical terms are sometimes necessary. But the report should still explain conditions in plain language so that buyers, boards, lenders, and investors can understand the practical meaning.

A report that sounds technical but does not communicate clearly is not useful.

The client should not need to be a roofer to understand that poor drainage may shorten roof life. They should not need to be an HVAC contractor to understand that multiple aging RTUs may create capital replacement risk. They should not need to be an electrician to understand that open electrical components should be corrected by a qualified professional.

Plain language does not mean oversimplified.

It means the report respects the reader’s need to make decisions.

Narrative Reporting Has Value

Checklist reports can be efficient, but commercial properties often require more explanation.

A checkbox may identify that a condition exists. A narrative explains why it matters.

For complex commercial properties, narrative reporting can be especially useful because conditions often overlap. A roof drainage problem may connect to exterior wall damage. HVAC equipment may affect roof condition. Site drainage may affect slab movement. Plumbing leaks may affect tenant spaces below. Deferred maintenance may show up across several systems.

A narrative report can explain those relationships.

That is important because commercial buildings do not fail in neat categories. Systems interact. Problems compound. Deferred maintenance spreads.

A strong narrative helps the client understand the story of the building.

That story is often what matters most.

Final Thoughts

A commercial inspection report should help people make decisions.

It should not be a generic defect list. It should not be vague. It should not bury limitations. It should not treat minor maintenance items and major capital risks as if they carry the same weight.

A useful commercial report should identify visible conditions, explain why they matter, document limitations, recognize deferred maintenance patterns, recommend specialist evaluation when needed, and help buyers, lenders, boards, trustees, investors, and property owners understand the physical risk attached to the property.

The report should be clear enough for people who were not present at the inspection to understand the major concerns.

That is the standard commercial clients should expect.

Because in commercial real estate, the report is not just paperwork.

It is part of the decision.

Need a Commercial Property Inspection Report That Supports Real Due Diligence?

Upchurch Inspection provides commercial property inspections and Property Condition Assessments for buyers, investors, lenders, trustees, boards, property owners, and real estate professionals throughout the Mid-South.

We help clients document visible building conditions, deferred maintenance, major system risks, scope limitations, and recommended next steps before closing, refinancing, budgeting, or major investment.

For commercial buildings, churches, campuses, warehouses, multifamily properties, offices, retail spaces, industrial properties, and mixed-use assets, we can help determine the right inspection scope and reporting format for the decision being made.

To discuss a commercial inspection or Property Condition Assessment, contact Upchurch Inspection.