A commercial buyer should be very careful about ordering a “home inspection” on a commercial building.

That does not mean a home inspector cannot inspect commercial property. Many competent inspectors do both residential and commercial work. The problem is not the person’s background. The problem is the scope.

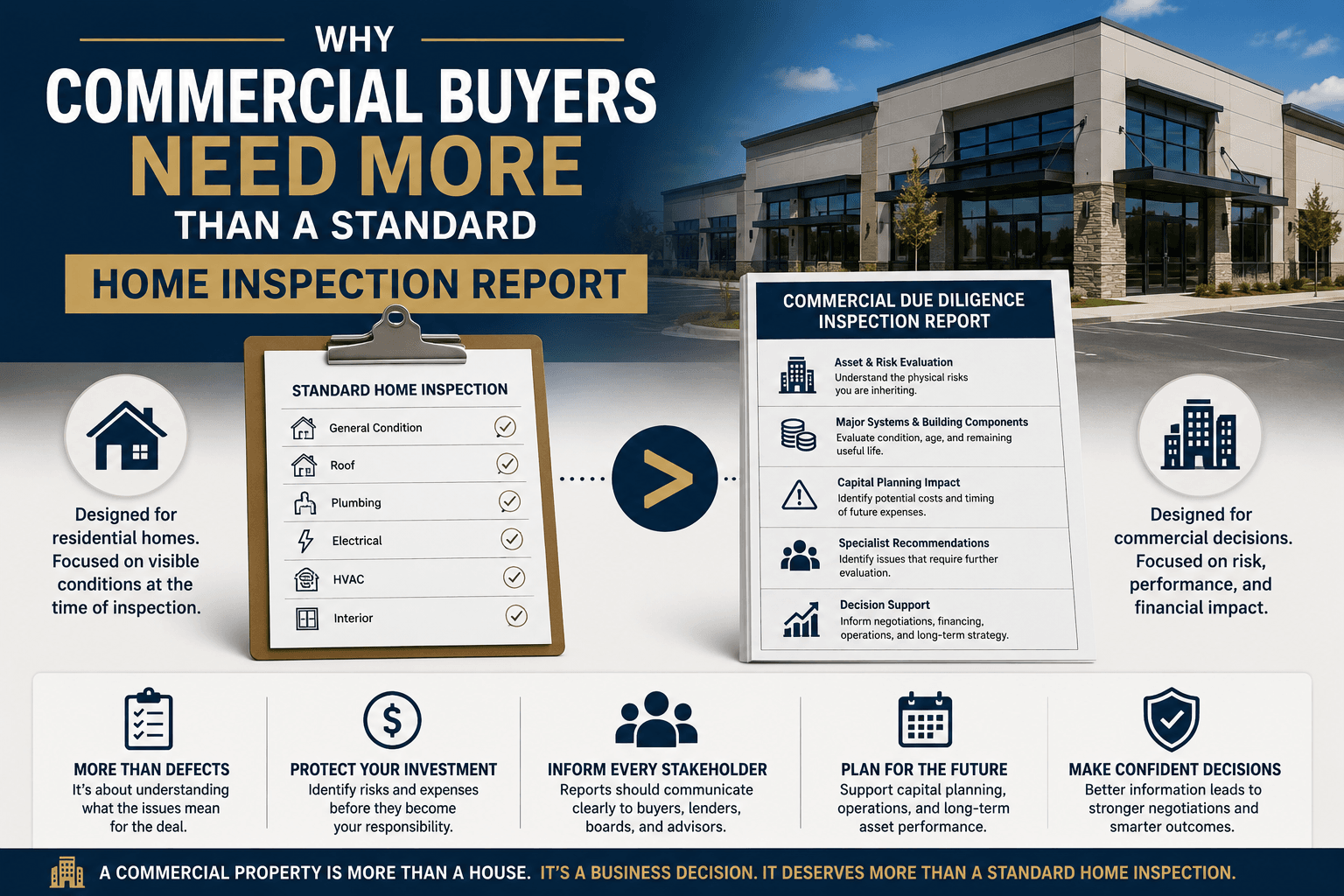

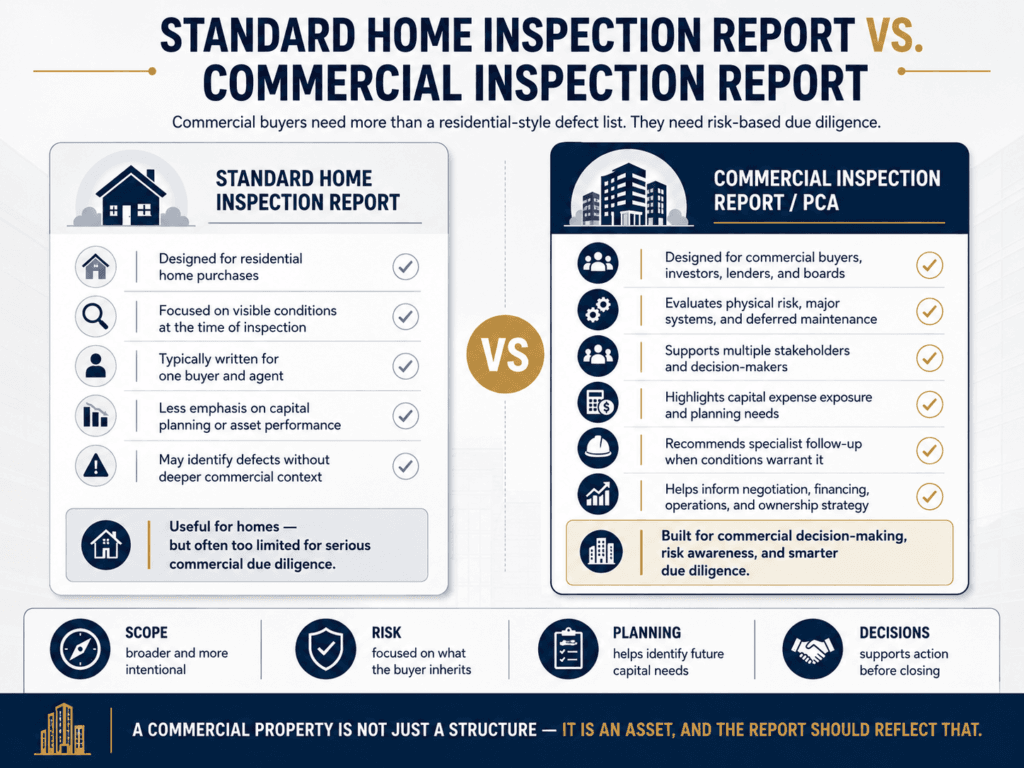

A standard residential home inspection is designed around a residential buyer, a residential structure, and residential expectations. It is generally focused on the condition of a house and its visible systems at the time of inspection.

Commercial due diligence is different.

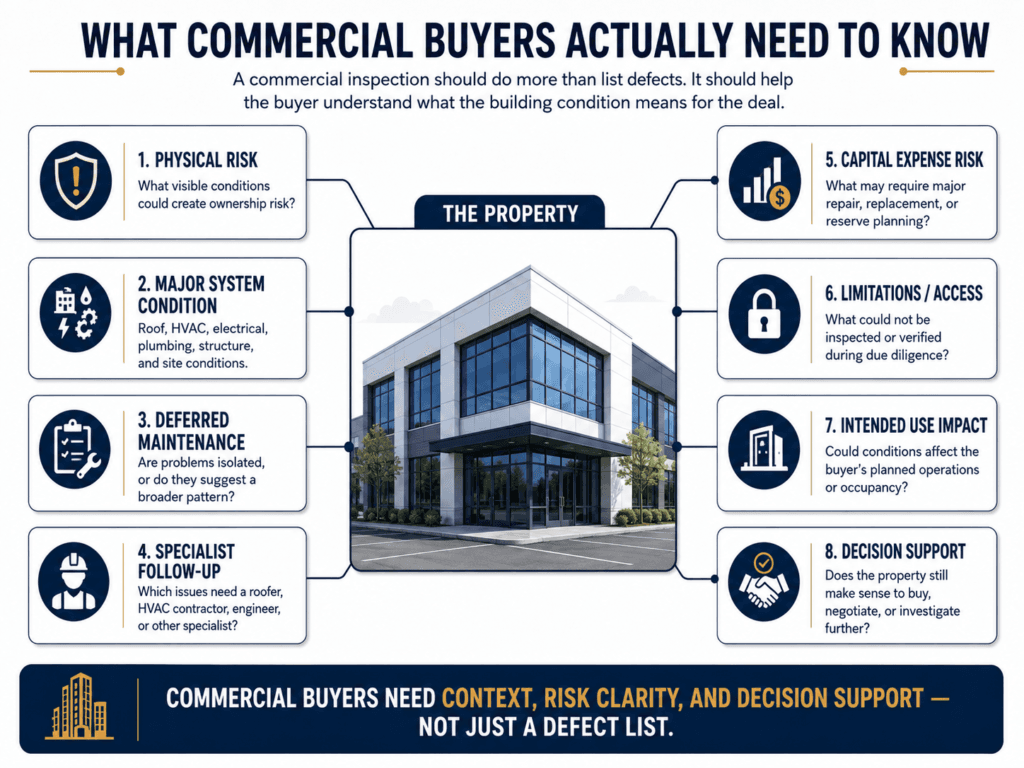

A commercial buyer is not just asking whether the building has defects. They are asking what kind of physical risk they are inheriting, what major systems may affect the deal, what conditions may require specialist evaluation, and what capital expenses may be waiting after closing.

That is why a standard home inspection report is usually not enough for a serious commercial acquisition.

Commercial real estate needs a different kind of conversation.

A Commercial Building Is an Asset, Not Just a Structure

A house is personal. A commercial building is financial.

That may sound blunt, but it matters.

A homebuyer is usually trying to understand whether the property is safe, functional, and reasonably maintained. A commercial buyer may care about those things too, but the purpose of the purchase is often different. The building may be intended to produce income, support business operations, house tenants, serve a congregation, hold inventory, support employees, satisfy a lender, or fit into a larger investment strategy.

That changes the inspection.

The buyer is not only evaluating walls, roofs, HVAC systems, plumbing, and electrical components. They are evaluating whether the physical condition of the property supports the business decision behind the purchase.

A roof defect on a house may affect repair negotiations. A roof defect on a commercial building may affect financing, tenant operations, insurance, capital reserves, and whether the deal works at all.

An aging HVAC system in a house may be a near-term replacement concern. Ten aging rooftop units on a commercial property may be a capital planning problem.

A cracked driveway at a house may be a maintenance item. A deteriorated commercial parking lot may create drainage problems, trip hazards, customer complaints, accessibility concerns, and a major resurfacing expense.

The same type of defect carries a different weight in commercial real estate because the building is tied directly to money, operations, liability, and long-term asset performance.

The Problem With Treating Commercial Property Like a House

A standard residential inspection report can be useful within its intended context. The issue begins when that same style of report is used for a commercial property without adjusting the scope, language, and purpose.

Commercial buildings are often larger, more complex, and more varied than houses. They may include flat or low-slope roofs, rooftop HVAC units, fire separation concerns, commercial electrical service, tenant improvements, parking lots, drainage systems, loading areas, common areas, multiple restrooms, kitchens, offices, retail spaces, warehouse sections, exterior stairs, accessibility-related features, and specialized mechanical systems.

A house usually has one main use. A commercial property may have several.

A church may include a sanctuary, classrooms, offices, kitchens, fellowship halls, storage areas, daycare spaces, and multiple additions from different decades. A small retail center may include separate tenant spaces with different build-out histories. A warehouse may have office space, loading doors, slab concerns, high-bay areas, and electrical requirements tied to operations. A multifamily property may have repeated systems across numerous units, where the important question is whether defects are isolated or systemic.

A residential-style inspection can miss the bigger point because it may focus too much on individual defects and not enough on commercial risk.

The buyer does not just need a list of things that are wrong.

The buyer needs to understand what those conditions mean.

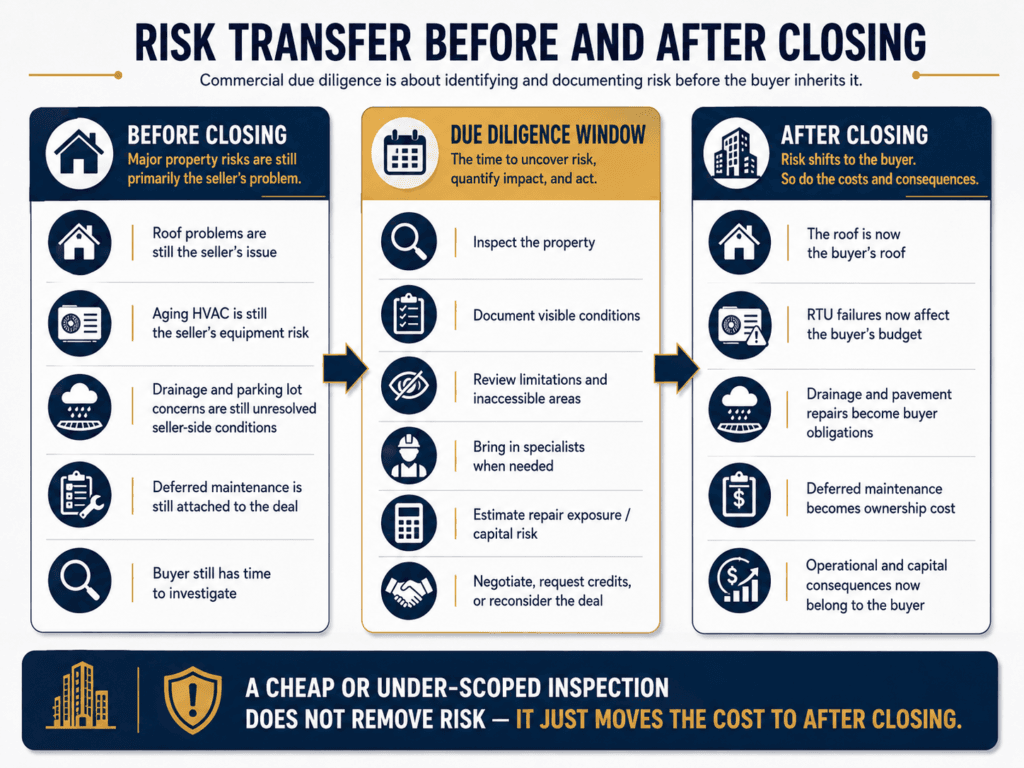

Commercial Due Diligence Is About Risk Transfer

Before closing, risk still belongs mostly to the seller.

After closing, it belongs to the buyer.

That is the entire reason commercial due diligence matters.

A buyer may have a limited inspection period to understand the property. During that window, the buyer needs to identify visible concerns, review documentation, request specialist evaluations when needed, evaluate repair exposure, and decide whether the property still makes sense.

Once the deal closes, the conversation changes.

The old roof is now the buyer’s roof. The failing rooftop units are now the buyer’s equipment. The drainage problem is now the buyer’s site issue. The deteriorated parking lot is now the buyer’s capital expense. The repeated plumbing leaks are now the buyer’s tenant problem.

A commercial inspection or Property Condition Assessment is not just about finding defects. It is about documenting risk before that risk transfers.

That is why the scope matters.

A vague walkthrough may be enough to make a buyer feel informed. It is not always enough to protect the decision-making process.

The Report Needs to Serve More Than One Reader

In a residential inspection, the report is usually written for the buyer, and maybe the buyer’s agent.

In a commercial transaction, the report may be reviewed by several people who did not attend the inspection. That may include an investor, lender, attorney, broker, property manager, facilities director, trustee, business partner, board member, insurance representative, or future maintenance team.

That changes how the report should be written.

A commercial report should not rely on casual explanations given during the walkthrough. It should stand on its own. It should explain what was observed, why it matters, what limitations applied, and when further evaluation is recommended.

A sentence like “HVAC is old” may not be enough.

A more useful commercial observation would explain that several rooftop units appeared aged, visible deterioration was observed, maintenance records were not provided, and further evaluation by a qualified HVAC contractor is recommended before the end of the due diligence period because near-term repair or replacement costs may affect capital planning.

That kind of reporting supports decisions.

Commercial clients need more than a defect label. They need context.

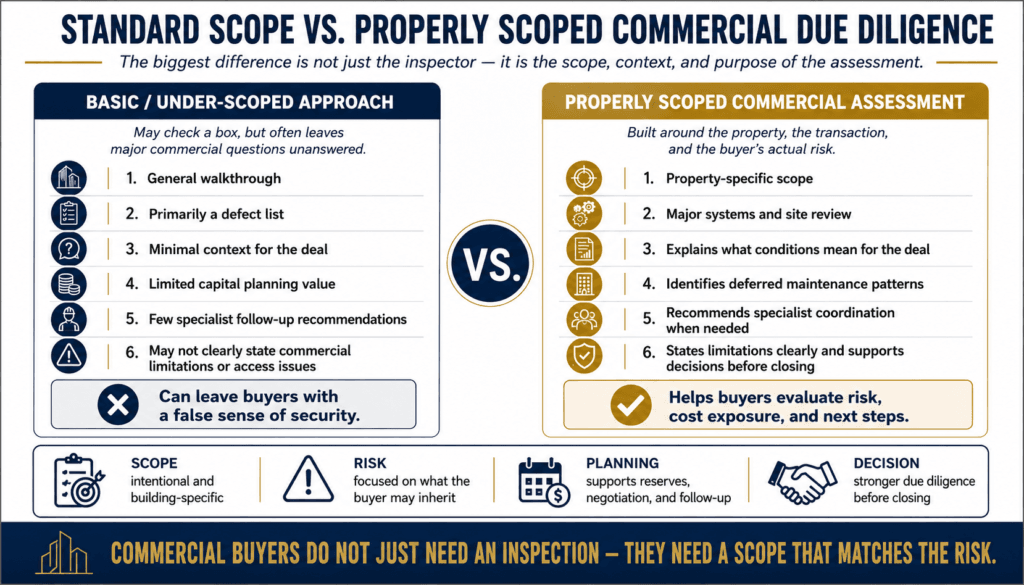

Standard of Care Starts With the Right Scope

The phrase “standard of care” gets thrown around, but in practical terms, it starts with matching the inspection scope to the property and the client’s needs.

A small office condo does not require the same scope as a multi-building church campus. A warehouse does not carry the same risk profile as a daycare. A four-unit apartment building is not the same as a 100-unit multifamily property. A vacant retail building is not the same as a fully occupied medical office.

The inspector and client need to be clear about what is being done.

Is this a general commercial inspection? Is it a limited-scope review? Is it an ASTM-style Property Condition Assessment? Will cost opinions be included? Are specialists being coordinated? Will the roof be accessed? Are all tenant spaces available? Will the report include reserve planning? Are environmental concerns excluded? Are elevators, fire suppression systems, kitchen equipment, specialized machinery, or security systems outside the scope?

These questions are not paperwork details. They define what the client is actually buying.

A commercial buyer who needs a lender-facing due diligence report may not be well served by a basic walkthrough. A buyer purchasing a small, low-risk building may not need a full formal PCA. The right answer depends on the property, the transaction, and the risk tolerance of the client.

But the scope should be intentional.

That is the difference between checking a box and performing real due diligence.

ASTM E2018 and Why It Matters

Some commercial clients need a Property Condition Assessment guided by ASTM E2018, the standard commonly associated with baseline commercial PCAs.

An ASTM-style PCA is not the same thing as a residential home inspection. It is structured around commercial due diligence and typically focuses on major building systems, site components, physical deficiencies, and opinions about probable costs or future capital needs when included in the agreed scope.

Not every commercial inspection must be an ASTM E2018 PCA. But commercial buyers should understand the difference.

A general commercial inspection may identify visible deficiencies and provide a practical overview of the property. A PCA may be more formal, with greater emphasis on physical deficiencies, system condition, remaining useful life, and capital planning. Some clients may need a hybrid approach depending on the property and transaction.

The important point is not to use a fancy label.

The important point is to make sure the assessment answers the buyer’s actual questions.

For many commercial buyers, those questions are not answered by a standard home inspection format.

Commercial Properties Often Require Specialist Coordination

No single inspector can fully evaluate every specialized system in every commercial building.

That is not a weakness. That is reality.

Commercial properties may include complex roofing systems, rooftop HVAC equipment, commercial electrical service, fire suppression systems, elevators, commercial kitchens, boilers, chillers, sewer systems, drainage structures, retaining walls, environmental concerns, structural issues, and specialty equipment.

A good commercial assessment should identify when further evaluation is needed.

For example, if multiple rooftop units are aged and deteriorated, an HVAC contractor may need to evaluate them before closing. If a low-slope roof shows ponding, open seams, soft areas, or prior repairs, a commercial roofing contractor may need to provide a repair or replacement opinion. If cracks, settlement, deflection, or structural movement are observed, a structural engineer may be needed. If the property has environmental concerns, a separate environmental professional may be appropriate.

A commercial inspection should not pretend to be everything.

It should help direct the buyer toward the right next step.

That is one of the most important parts of due diligence: knowing when a visible condition is serious enough to bring in a specialist before the inspection period expires.

Commercial Reports Should Address Deferred Maintenance

Deferred maintenance is one of the biggest issues in commercial property.

It does not always show up as one dramatic defect. More often, it appears as a pattern. Aging roof sealants. Poor drainage. Dirty mechanical equipment. Damaged exterior finishes. Cracked pavement. Stained ceiling tiles. Rusted equipment. Patched plumbing. Missing electrical covers. Poor access. Old repairs. Tenant spaces maintained at different levels.

A residential-style report may list those items separately.

A stronger commercial report explains the pattern.

That matters because deferred maintenance affects the economics of ownership. It tells the buyer whether the property has been maintained proactively or operated on a patch-and-react basis.

There is a big difference between a building with normal age-related wear and a building where every major system appears to have been pushed as far as possible before sale.

Commercial buyers need that distinction.

The report should help them understand whether they are buying a clean asset with ordinary maintenance needs or inheriting years of neglected repairs.

Capital Expense Risk Should Be Part of the Conversation

A commercial buyer may not need exact repair pricing from the inspector. In many cases, contractor estimates are required for that.

But the inspection should still help identify where capital expense risk may exist.

The roof may be near the end of its useful life. Several RTUs may be aged. The parking lot may need resurfacing. Plumbing problems may appear across multiple areas. Electrical service may be inadequate for the buyer’s intended use. Drainage may be affecting the site and building envelope.

These are not just inspection findings. They are potential capital events.

A report that fails to communicate capital risk may leave the buyer with a false sense of security.

The commercial client needs to know which issues may affect budgeting, negotiation, lender discussions, or post-closing ownership. Some defects are minor. Some are maintenance items. Some are expensive, urgent, or strategic.

A good commercial report helps separate those categories.

The Inspection Should Fit the Intended Use

Commercial properties are often purchased for a specific business or investment purpose.

That intended use matters.

A warehouse being used for basic storage has different concerns than a warehouse being converted into manufacturing space. A former retail building being converted into a daycare has different concerns than a retail building staying retail. A church campus has different concerns than a small office building. A medical office has different concerns than a vacant shell.

The inspection should consider whether the observed conditions may affect the buyer’s planned use.

That does not mean the inspector is approving the use, performing design work, or guaranteeing code compliance. It means the report should recognize obvious physical conditions that may interfere with the client’s plans or warrant further evaluation.

If the buyer needs heavy electrical capacity, the electrical system matters differently. If the buyer needs reliable cooling for patients, tenants, or children, HVAC performance matters differently. If the buyer expects public access, parking lot and walkway conditions matter differently. If the buyer plans renovation, structural limitations, moisture conditions, and previous modifications matter differently.

A standard home inspection report is rarely designed to think this way.

Commercial due diligence should.

Accessibility and Life Safety Need Careful Language

Commercial buyers often ask about ADA compliance, life safety, fire protection, and code issues.

These are important topics, but they require careful scope language.

A commercial inspection is not automatically a full ADA compliance audit, fire marshal inspection, building code inspection, or architectural review. Those are separate services requiring specific expertise and authority.

That said, visible accessibility-related and life-safety concerns can still be very important.

A report may note obvious issues involving exterior routes, ramps, stairs, handrails, guards, emergency lighting, exit signage, smoke alarms, carbon monoxide alarms where applicable, electrical safety, fire separation concerns, or unsafe walking surfaces. When appropriate, the report should recommend further evaluation by qualified professionals or local authorities.

This is another reason a residential-style report is not enough.

Commercial properties interact with the public, tenants, employees, visitors, patients, children, congregation members, or customers. The risk environment is different.

The report needs to be clear about what was observed, what was not evaluated, and what should be reviewed further.

Limitations Matter More in Commercial Work

Every inspection has limitations.

In commercial work, those limitations can be significant.

The roof may not be safely accessible. Some tenant spaces may be locked. Mechanical equipment may be turned off. Electrical panels may be blocked. Maintenance rooms may be inaccessible. Stored materials may hide walls, floors, or equipment. Weather may limit evaluation. Utilities may be off. Documentation may not be provided. Some systems may require specialized testing outside the scope of the inspection.

A good commercial report should state limitations clearly because limitations affect risk.

If half the tenant spaces were inaccessible, the buyer needs to know that. If the roof was not accessed, that matters. If maintenance records were not available, that matters. If specialized systems were excluded, that matters.

Limitations are not just legal disclaimers.

They are part of the due diligence picture.

A buyer may need to request additional access, extend the inspection period, bring in specialists, or adjust risk assumptions based on what could not be verified.

The Cheapest Report Can Become the Most Expensive Decision

Commercial buyers are often managing many closing costs at once. It can be tempting to choose the lowest inspection fee available.

That may be fine for a low-risk property with a simple scope.

But for larger, older, or more complex properties, under-scoping the inspection can be an expensive mistake.

A cheap report that fails to identify roof risk, aging mechanical systems, drainage problems, electrical concerns, plumbing patterns, or deferred maintenance does not save money. It just moves the cost to after closing.

The buyer may save a small amount on the inspection and inherit a six-figure problem.

That is not good due diligence.

The inspection fee should make sense in relation to the size, complexity, and financial risk of the property. A multi-building campus, industrial facility, church, multifamily property, or large commercial asset deserves a scope that matches the decision being made.

The larger the potential downside, the more important the due diligence.

A standard home inspection report may identify defects. A properly scoped commercial assessment should help the buyer understand risk, cost, and what those defects mean for the deal.

-Wesley Upchurch, Upchurch Inspection

What a Strong Commercial Report Should Do

A strong commercial report should help the client understand the property as an asset.

It should document visible conditions, explain major concerns, identify patterns of deferred maintenance, point out limitations, recommend specialist evaluation where needed, and help the buyer think clearly about post-closing obligations.

It should not simply copy a residential format and change the word “home” to “commercial building.”

The report should be written for decision-making.

That means the findings should be understandable to someone who may not be a contractor but still needs to make a serious financial decision. It should be technical enough to be useful, but clear enough for buyers, lenders, trustees, investors, and property owners to act on.

That is the balance commercial clients need.

Final Thoughts

Commercial buyers need more than a standard home inspection report because commercial buildings carry different risks.

The issue is not whether the building has defects. Every building has defects. The issue is whether those defects affect the financial, operational, or strategic decision behind the purchase.

A residential-style report may tell a buyer what is wrong with a building.

A properly scoped commercial inspection or Property Condition Assessment should help the buyer understand what those conditions mean.

That is the difference.

Commercial due diligence is about risk, cost, documentation, and decision-making. It is about identifying visible concerns before the buyer inherits them. It is about knowing when to bring in specialists. It is about understanding deferred maintenance before it becomes the new owner’s problem.

A commercial property is not just a structure.

It is an asset.

And an asset deserves an assessment that matches the risk.

Need a Commercial Property Inspection or PCA?

Upchurch Inspection provides commercial property inspections and Property Condition Assessments for buyers, investors, lenders, trustees, property owners, and real estate professionals throughout the Mid-South.

We help clients evaluate commercial buildings with attention to visible system condition, deferred maintenance, major capital risks, scope limitations, and practical decision-making before closing or major investment.

For commercial buildings, multifamily properties, churches, campuses, offices, warehouses, retail spaces, and mixed-use properties, we can help determine the right inspection scope for the deal.

To discuss a commercial property inspection or Property Condition Assessment, contact Upchurch Inspection.