Buying commercial property is not the same as buying a house.

A residential buyer is usually trying to answer a fairly simple question: Is this home safe, functional, and worth what I am paying for it?

A commercial buyer has a bigger problem.

They need to know what physical risks they are inheriting, what major systems may require near-term repair or replacement, and whether the property’s condition supports the financial assumptions behind the deal.

That is where a Property Condition Assessment, often called a PCA, becomes valuable.

A commercial building may look acceptable during a walkthrough. The roof may not be actively leaking. The HVAC units may be running. The parking lot may be usable. The electrical service may appear functional. But that does not mean the property is free of major capital risk.

A PCA is designed to help commercial buyers, investors, lenders, trustees, and property owners better understand the physical condition of a property before closing, refinancing, budgeting, or making a major ownership decision.

At Upchurch Inspection, we view commercial assessments as a form of risk management. The goal is not just to list defects. The goal is to help clients understand what conditions may affect cost, operation, negotiation, safety, maintenance planning, and long-term ownership.

What Is a Property Condition Assessment?

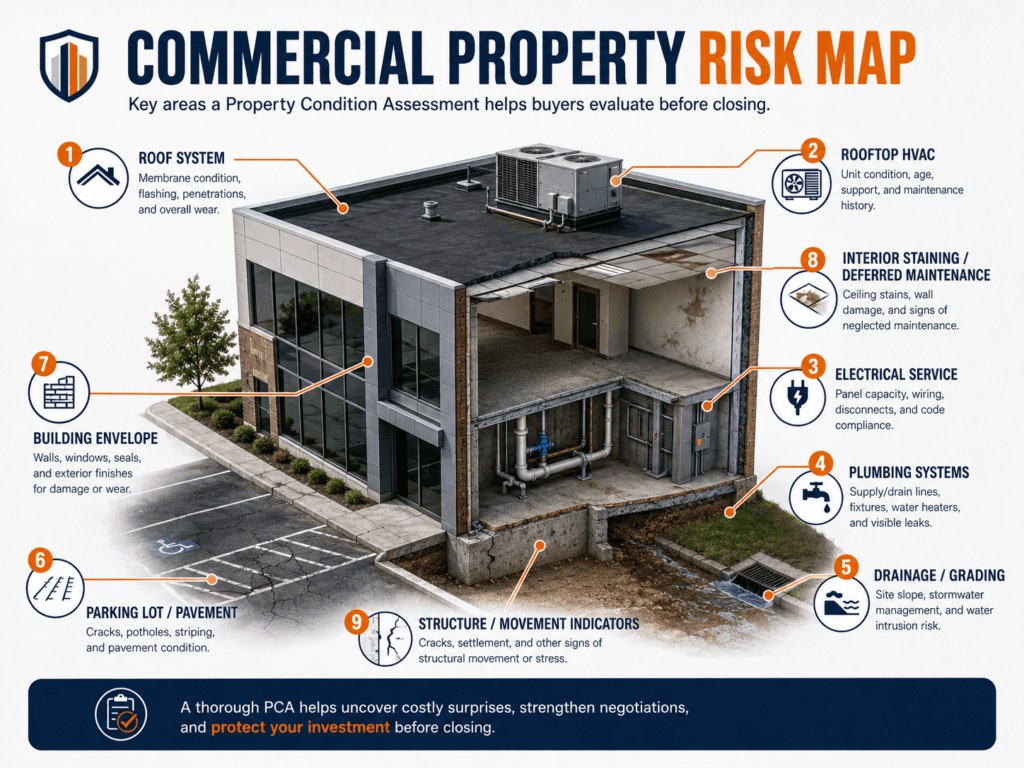

A Property Condition Assessment is a commercial due diligence inspection focused on the major physical components of a building and site.

Depending on the property and scope of work, a PCA may include review of:

- Roofing systems

- Exterior walls and building envelope

- Structural components

- Site drainage and grading

- Parking lots, sidewalks, and paved areas

- HVAC systems

- Electrical systems

- Plumbing systems

- Interior spaces

- Life-safety observations

- Accessibility-related observations

- General maintenance conditions

- Signs of deferred maintenance

- Opinions about remaining useful life

- Recommendations for further specialist evaluation where needed

A PCA is not the same thing as a residential home inspection. It is also not the same as a code inspection, engineering study, environmental assessment, or full design review.

The purpose is to provide a practical, documented overview of the property’s visible and readily observable condition, with emphasis on major systems, physical risk, and potential capital expense concerns.

For commercial buyers, that distinction matters.

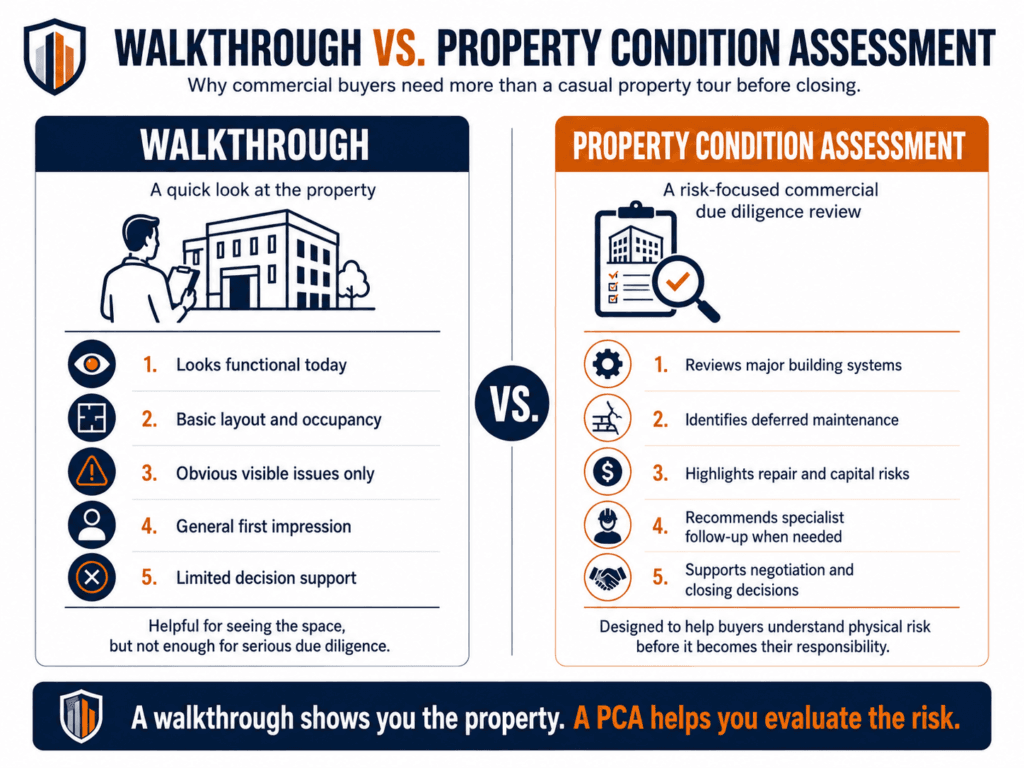

Why Commercial Buyers Need More Than a Walkthrough

Many commercial deals start with a basic walkthrough.

The buyer walks the property. The broker points out the square footage, tenant layout, rent potential, location, and improvements. The building may seem functional enough.

But a walkthrough is not due diligence.

A walkthrough usually does not answer questions like:

- How old are the rooftop HVAC units?

- Are the roof drains working properly?

- Is there evidence of chronic ponding water?

- Are there signs of structural movement?

- Is the electrical system adequate for the current or intended use?

- Are plumbing problems isolated or systemic?

- Is the parking lot nearing major repair or replacement?

- Are there signs of deferred maintenance across multiple systems?

- Will the buyer need to budget for major repairs within the next few years?

That is the difference between looking at a building and evaluating a building.

Commercial buyers are not just buying walls, roofs, and mechanical systems. They are buying future obligations. Every aging roof, failing HVAC unit, deteriorated parking lot, and hidden drainage problem becomes part of the financial reality of owning that asset.

A proper commercial assessment helps bring those risks into the open before the deal closes.

The Real Question: What Financial Liability Are You Inheriting?

In commercial real estate, defects are not just repair items. They are financial events.

A roof concern on a small house may be a few thousand dollars. A roof issue on a commercial building can become a six-figure capital expense.

An aging residential HVAC system may be inconvenient. A failing commercial rooftop unit can affect tenants, operations, lease obligations, comfort complaints, and emergency replacement costs.

A cracked driveway at a house may be cosmetic. A deteriorated commercial parking lot may create drainage issues, trip hazards, tenant complaints, and major resurfacing costs.

This is why commercial due diligence needs to be viewed through a capital planning lens.

The buyer is not only asking, “What is wrong?”

They are asking:

What is this going to cost me after closing?

A strong commercial assessment helps identify conditions that may affect:

- Purchase negotiations

- Repair credits

- Capital reserve planning

- Lender review

- Insurance concerns

- Tenant obligations

- Lease assumptions

- Operational planning

- Board or investor approval

- Long-term asset management

That is where the real value is.

Deferred Maintenance Is Often the Bigger Problem

One of the most important things we look for during a commercial assessment is deferred maintenance.

Deferred maintenance does not always show up as one dramatic defect. More often, it appears as a pattern.

For example:

- Roof sealants are aged and failing

- Gutters or internal drains are not properly maintained

- HVAC units have dirty coils, damaged insulation, rust, and missing service documentation

- Exterior caulking is deteriorated

- Parking lot cracks have gone unsealed

- Drainage is pushing water toward the building

- Electrical panels show old labeling, abandoned wiring, or amateur modifications

- Plumbing fixtures show repeated leakage or patchwork repairs

- Interior finishes show recurring staining or moisture damage

Individually, some of these items may look manageable.

Together, they can tell a different story.

They may suggest that the property has been operated reactively instead of proactively. For a buyer, that matters because deferred maintenance does not disappear after closing. It transfers.

The new owner inherits the consequences.

Commercial Roofs: A Major Due Diligence Concern

Commercial roofing is one of the most important areas of a Property Condition Assessment.

A roof can look acceptable from the ground and still have significant concerns. Commercial roofs often include membranes, seams, drains, scuppers, parapet walls, penetrations, mechanical curbs, flashing details, and roof-mounted equipment.

Common concerns may include:

- Ponding water

- Damaged or aged membrane

- Open seams

- Deteriorated flashing

- Poor drainage

- Clogged roof drains

- Improper repairs

- Damaged coping

- Rusted metal components

- Soft or deteriorated roof areas

- Improperly sealed penetrations

- Evidence of prior leaks

For commercial buyers, the roof is not just a maintenance issue. It is a capital expense issue.

A roof near the end of its useful life can significantly affect the true cost of acquisition. Even if the seller says the roof “doesn’t leak,” that does not answer the buyer’s real question.

The real question is:

How much roof risk am I buying?

HVAC Systems and Rooftop Units

Commercial HVAC systems are another major capital concern.

Many commercial properties rely on rooftop units, split systems, package units, boilers, chillers, or other mechanical equipment depending on the building type and use.

During a commercial assessment, we are often looking for visible indicators such as:

- Approximate age of equipment

- General condition

- Rust or cabinet deterioration

- Damaged refrigerant line insulation

- Poor condensate management

- Improper clearances

- Missing service records

- Dirty coils

- Damaged ductwork

- Units that are not operating properly

- Evidence of piecemeal repair

- Mismatched equipment

- Lack of maintenance access

A commercial HVAC system may be running on the day of inspection but still represent a significant near-term expense.

That is why age, condition, maintenance history, and system type matter.

For buyers, HVAC findings can affect budgeting immediately. Replacing one rooftop unit may be manageable. Replacing several units across a retail center, office building, church campus, or multifamily property can change the financial picture of the deal.

Parking Lots, Drainage, and Site Conditions

Commercial buyers sometimes focus heavily on the building and underestimate the site.

That can be a mistake.

Parking lots, sidewalks, drainage systems, retaining walls, exterior stairs, ramps, curbs, and loading areas can carry major cost and liability concerns.

Common issues may include:

- Cracked asphalt

- Failed patching

- Poor drainage

- Ponding water

- Settlement

- Trip hazards

- Damaged curbs

- Deteriorated striping

- Inadequate slope

- Erosion

- Water collecting near the foundation

- Poorly maintained stormwater features

In the Mid-South, drainage is a recurring issue. Heavy rain, clay soils, poor grading, and deferred maintenance can create conditions where water repeatedly moves toward buildings instead of away from them.

Over time, that can affect foundations, slabs, crawlspaces, basements, masonry, parking areas, and interior finishes.

A commercial assessment should not ignore the site. The site is part of the asset.

Plumbing and Electrical Risks

Commercial plumbing and electrical systems can be difficult to fully evaluate without invasive testing or specialist review, but visible conditions still matter.

With plumbing, we may look for:

- Active leaks

- Old or mixed piping materials

- Poor repairs

- Water heater concerns

- Drainage issues

- Staining

- Corrosion

- Inadequate access

- Fixture problems

- Signs of systemic failures across multiple areas

In multifamily, older office, retail, restaurant, church, and institutional buildings, plumbing problems may not be isolated. A single leak may be one defect. Repeated staining, active repairs, and recurring fixture problems may suggest a broader maintenance pattern.

With electrical systems, common concerns may include:

- Open electrical defects

- Missing covers

- Improper wiring

- Double-tapped breakers

- Poor labeling

- Obsolete or aging equipment

- Damaged panels

- Unsafe modifications

- Inadequate service for intended use

- Lack of GFCI protection where expected

- Exposed wiring

- Abandoned wiring

For commercial buyers, electrical concerns should be taken seriously because they can affect safety, insurability, tenant use, and future improvements.

The Importance of Scope

One of the biggest mistakes commercial buyers make is assuming every inspection is the same.

It is not.

A commercial assessment should be scoped according to the property type, client needs, building complexity, and intended use.

A small office condo does not need the same approach as a 60,000-square-foot industrial building. A church campus with multiple buildings, kitchens, classrooms, sanctuaries, flat roofs, parking lots, and older mechanical systems needs a different approach than a small retail storefront.

The scope may also need to include additional specialists, such as:

- Commercial roofing contractor

- HVAC contractor

- Electrical contractor

- Structural engineer

- Sewer camera provider

- Environmental consultant

- Fire protection contractor

- Elevator contractor

- Plumbing contractor

A good commercial inspector should know when a condition is within the assessment scope and when further evaluation is needed.

That is not weakness. That is proper due diligence.

The point is not to pretend one person can fully evaluate every specialized system in a complex commercial asset. The point is to identify visible risk, document concerns, and help the client decide where deeper evaluation is justified.

What a Commercial Report Should Help the Client Understand

A commercial inspection report should do more than say something is “defective.”

It should help the client understand the significance of the condition.

A useful report may help answer:

- What was observed?

- Why does it matter?

- Is this a maintenance item or a major concern?

- Does it suggest deferred maintenance?

- Could it affect operation or occupancy?

- Is specialist evaluation recommended?

- Could this affect negotiation?

- Is this likely to become a capital expense?

- Should this be reviewed before the inspection period expires?

This is especially important when the report is being reviewed by multiple decision-makers.

Commercial deals often involve more than one person. The report may be read by buyers, attorneys, brokers, lenders, trustees, partners, investors, facility managers, or board members.

That means the report needs to be clear, organized, and practical.

It should not be written only for the person who walked the property. It should be written for the people who have to make decisions based on the findings.

ASTM E2018 and Commercial Due Diligence

Some commercial clients request assessments that follow the general framework of ASTM E2018, the commonly referenced standard for baseline Property Condition Assessments.

An ASTM-style PCA is designed to provide a structured review of major building systems and site components, often including opinions regarding physical deficiencies and potential costs.

Not every commercial inspection needs to be a full ASTM PCA. Some clients need a limited-scope commercial inspection. Others need a more formal due diligence assessment with cost opinions, reserve planning, and specialist coordination.

The important point is that the scope should match the client’s risk.

For a low-risk, small commercial property, a simpler commercial inspection may be appropriate.

For a larger acquisition, institutional property, multifamily portfolio, industrial facility, or lender-involved transaction, a more formal Property Condition Assessment may be the better fit.

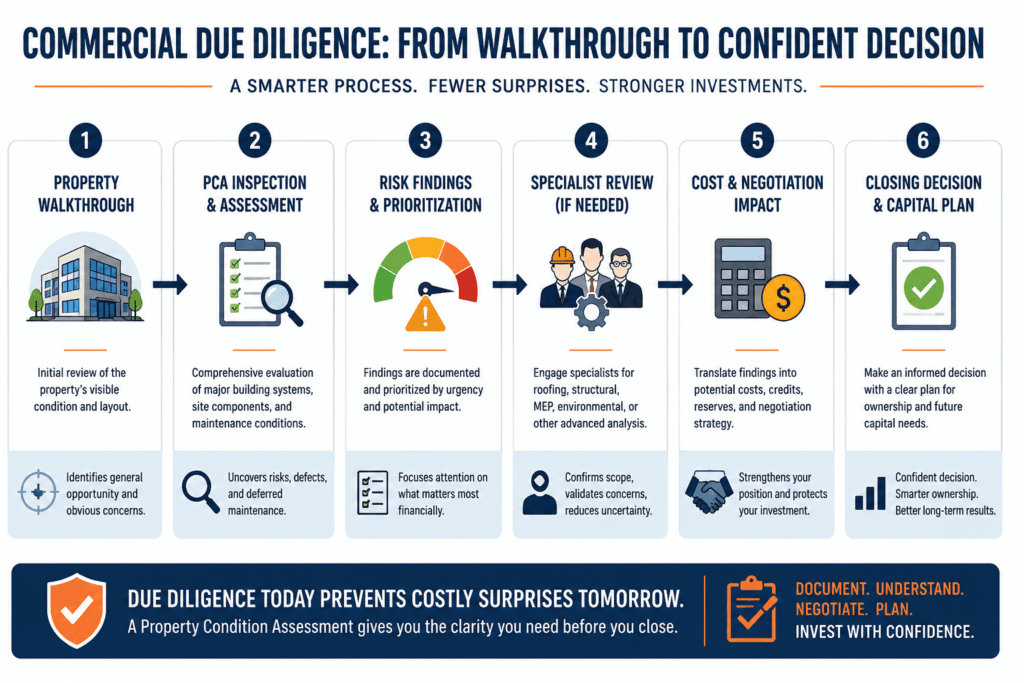

Commercial Due Diligence Is About Defensible Decision-Making

A commercial inspection should not be treated as a box to check.

It should support a defensible decision.

That decision may be:

- Move forward with the purchase

- Renegotiate the price

- Request repairs

- Require seller concessions

- Extend the due diligence period

- Bring in specialists

- Adjust capital reserves

- Reconsider the deal

- Develop a maintenance plan after closing

In commercial real estate, uncertainty is expensive. The more a buyer understands before closing, the better positioned they are to manage risk.

The inspection does not eliminate risk. No inspection can.

But a properly scoped commercial assessment can help make the risk visible.

Why Local Experience Matters

Commercial buildings in the Mid-South face specific regional conditions.

In West Tennessee, North Mississippi, Arkansas, Missouri, and surrounding areas, we regularly see how climate and site conditions affect buildings over time.

Common regional factors include:

- Heavy rainfall

- High humidity

- Clay soils

- Poor drainage

- Crawlspace and moisture issues

- Flat and low-slope roof challenges

- Aging mechanical systems

- Older masonry buildings

- Renovated commercial spaces with mixed-quality work

- Deferred maintenance in long-held properties

- Older multifamily and institutional buildings with systemic issues

A commercial assessment should account for how buildings actually age in the region where they are located.

A roof, HVAC system, parking lot, or drainage issue in the Mid-South may carry different practical concerns than the same system in a different climate.

Local context matters.

Commercial due diligence is not just about finding defects. It is about understanding the financial risk attached to the building before that risk becomes yours.

-Wes Upchurch

Final Thoughts

A Property Condition Assessment is not just about finding defects.

It is about helping commercial buyers understand risk before they inherit it.

The most expensive problems in commercial real estate are not always the ones that are obvious during a walkthrough. They are often the conditions hiding in plain sight: aging rooftop units, tired roof systems, drainage problems, deferred maintenance, electrical concerns, plumbing patterns, failing pavement, and building systems that are still working but nearing the end of their practical life.

A commercial buyer does not need a generic checklist.

They need a clear assessment of the property’s physical condition, major risks, and potential capital concerns.

That is what a properly scoped commercial inspection or Property Condition Assessment is designed to provide.

Need a Commercial Property Assessment?

Upchurch Inspection provides commercial property inspections and Property Condition Assessments for investors, buyers, owners, lenders, trustees, and real estate professionals throughout the Mid-South.

We help clients evaluate commercial buildings with a focus on physical condition, deferred maintenance, major system risk, and practical decision-making before closing or major investment.

To schedule a commercial inspection or discuss the right scope for your property, contact Upchurch Inspection.