TL;DR:

- A property condition assessment is a critical financial tool that quantifies physical risks into capital cost projections and negotiation leverage. It goes beyond a home inspection by evaluating systemic issues, long-term costs, and compliance standards crucial for commercial and multifamily transactions. Understanding and properly interpreting a PCA helps investors and lenders manage future expenses, avoid costly surprises, and make informed decisions.

A property condition assessment is one of the most misused tools in real estate. Most buyers treat it like a pass/fail inspection, waiting to see if a property “passes” before moving forward. That framing costs money. A well-executed assessment is actually a financial risk-measurement tool, one that translates physical building conditions into capital cost projections and negotiating leverage. Whether you’re acquiring a commercial asset, refinancing a multifamily portfolio, or making your first significant investment purchase, understanding how this process works is the difference between a sound decision and a costly surprise.

Table of Contents

- Key takeaways

- What a property condition assessment actually covers

- When a PCA is critical in real estate transactions

- Reading and interpreting the PCA report

- Common pitfalls when commissioning a PCA

- How PCAs compare to home inspections and appraisals

- My take on PCAs in real estate investing

- Get a PCA that actually protects your investment

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Not a pass/fail inspection | A property condition assessment quantifies physical risk in financial terms for negotiation and planning. |

| ASTM E2018-24 sets the standard | Compliant assessments include mandatory cost tables covering immediate repairs and 12-year capital forecasts. |

| PCA differs from a home inspection | PCAs cover financial modeling and building-wide systems; standard home inspections focus on visible defects only. |

| Systemic issues carry hidden costs | Clusters of deferred maintenance signal deeper problems that multiply future repair expenses exponentially. |

| Report quality determines usefulness | Noncompliant PCA reports can stall loan closings and fail to meet GSE requirements for multifamily financing. |

What a property condition assessment actually covers

Most people conflate a property condition assessment with a standard home inspection. They’re related but not interchangeable. A PCA is a formal physical and document-based evaluation of a property’s condition, governed by the ASTM E2018-24 standard, which establishes the minimum scope, procedures, and deliverables an assessor must follow to produce a credible, consistent report.

The scope goes well beyond what a typical residential inspection covers. A PCA examines:

- Structural systems, including foundation, framing, and load-bearing components

- Mechanical, electrical, and plumbing (MEP) systems, with attention to service life and deferred maintenance

- Site improvements, such as parking lots, drainage, and retaining walls

- Life safety systems, including fire suppression, egress paths, and emergency lighting

- Roof and envelope systems, evaluated for remaining useful life and water intrusion risk

The process itself involves four phases: a physical site inspection, interviews with property managers or owners, a review of available maintenance records and permits, and finally the preparation of a written Property Condition Report (PCR). Each phase feeds the next. What a property manager tells you about HVAC service history, for instance, directly shapes how an assessor estimates remaining useful life on that equipment.

Where a PCA differs from an appraisal is equally worth understanding. A licensed appraiser primarily focuses on market value, using comparable sales. They note the general condition but don’t provide detailed capital planning data. A PCA fills that gap. It tells you not just what a building is worth, but what it will cost to maintain over the next decade.

When a PCA is critical in real estate transactions

There are specific points in the real estate lifecycle where skipping a property condition assessment creates real financial exposure. Experienced investors know this. Here are the most common scenarios where a PCA is not optional:

- Commercial property acquisition. Lenders on commercial transactions routinely require a PCA before approving financing. The report directly influences underwriting decisions, loan terms, and reserve requirements.

- Multifamily refinancing. Government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac have strict requirements for PCAs on multifamily loans. Non-compliant reports can stall closings at the last moment.

- Value-add investment analysis. When an investor targets a distressed asset, the PCA is the document that separates genuine opportunity from a money pit. It puts hard numbers on the capital improvements required.

- Portfolio management and annual planning. Owners managing multiple properties use PCA data to prioritize capital expenditures across their portfolio, preventing reactive spending.

- Pre-sale preparation. Sellers who commission a PCA before listing can address deficiencies proactively, reducing price concessions during negotiations.

The financial protection a PCA provides is direct. When a report surfaces $400,000 in deferred maintenance on a property listed at $3.2 million, the buyer has documented leverage. That’s not a minor inspection note. That’s a renegotiation. A PCA’s financial forecasts become the foundation for purchase price adjustments, seller credits, and reserve escrow requirements built into the loan.

Beyond negotiations, a PCA protects lenders from funding assets with hidden capital deficiencies that would impair debt service over the loan term. That’s why compliance with the applicable standard isn’t optional for institutional transactions.

Reading and interpreting the PCA report

Once the assessment is complete, you’ll receive a Property Condition Report. Understanding its structure helps you extract real value from it rather than reading it as a list of problems to dread.

Every ASTM-compliant PCR contains two core financial tables:

| Table | Timeframe | Purpose |

|---|---|---|

| Immediate Repairs Table | Within 90 days | Captures urgent deficiencies requiring near-term capital outlay |

| Replacement Reserves Table | 12-year horizon | Projects long-term capital needs by building system |

The Immediate Repairs Table flags items with safety implications or accelerating deterioration that cannot wait. Think failed roofing membrane over occupied units, or an electrical panel operating beyond rated capacity. These aren’t cosmetic issues. They carry liability.

The Replacement Reserves Table is where long-term investment planning lives. It estimates remaining useful life for major building components, including HVAC units, roofing, elevators, parking surfaces, and plumbing infrastructure, then projects the probable replacement costs over a 12-year window. Capital expenditure forecasts over 12 years are not guesswork. They’re built on observed conditions, manufacturer service life data, and regional cost benchmarks.

Pro Tip: When reviewing a PCA report, pay close attention to systems within three to five years of their projected service life. A roof with four years of useful life remaining looks fine today. Factor replacement cost into your acquisition model, and it changes your return projections significantly.

Lenders use the reserve table to determine how much a borrower must escrow each month to cover projected capital expenses. That number affects your cash-on-cash return from day one. Investors who overlook it often find themselves cash-strapped three years into ownership when a major system fails prematurely.

Common pitfalls when commissioning a PCA

Getting a PCA is only valuable if the report you receive is credible, compliant, and thorough. Here is where many buyers and investors lose ground:

- Choosing the wrong firm. Not every inspection company produces ASTM E2018-24-compliant reports. For multifamily and commercial transactions, GSE-compliant assessments require firms with professional engineering credentials and specific report formats. Verify credentials before engaging.

- Accepting a report that only lists isolated defects. A PCA should identify patterns. Clusters of maintenance issues signal systemic neglect, where moisture intrusion combined with poor drainage is a classic example. One leaking roof drain is a repair. Five deferred maintenance items centered on water management is a systemic failure with exponentially higher long-term costs.

- Ignoring regulatory context. For HUD-related multifamily properties, the NSPIRE inspection protocol evaluates units, common areas, and the exterior as a combined score. A property score below 60 triggers mandatory full surveys and immediate correction requirements. Understanding this context shapes how you read condition data on HUD-assisted assets.

- Underestimating the report’s shelf life. PCA reports age. Most lenders consider a PCA valid for 12 months. If a transaction drags past that window, a refresh may be required, adding cost and delay. Build that timeline into your due diligence schedule.

Pro Tip: Ask your PCA provider directly whether their report format meets current GSE requirements before you engage them. A single yes-or-no question at the start can prevent a compliance problem weeks before your closing date.

Experienced investors also pay attention to how assessors describe uncertainty. Vague language around a building system’s condition is sometimes a signal that access was limited or records were unavailable. Follow up on those gaps before you close.

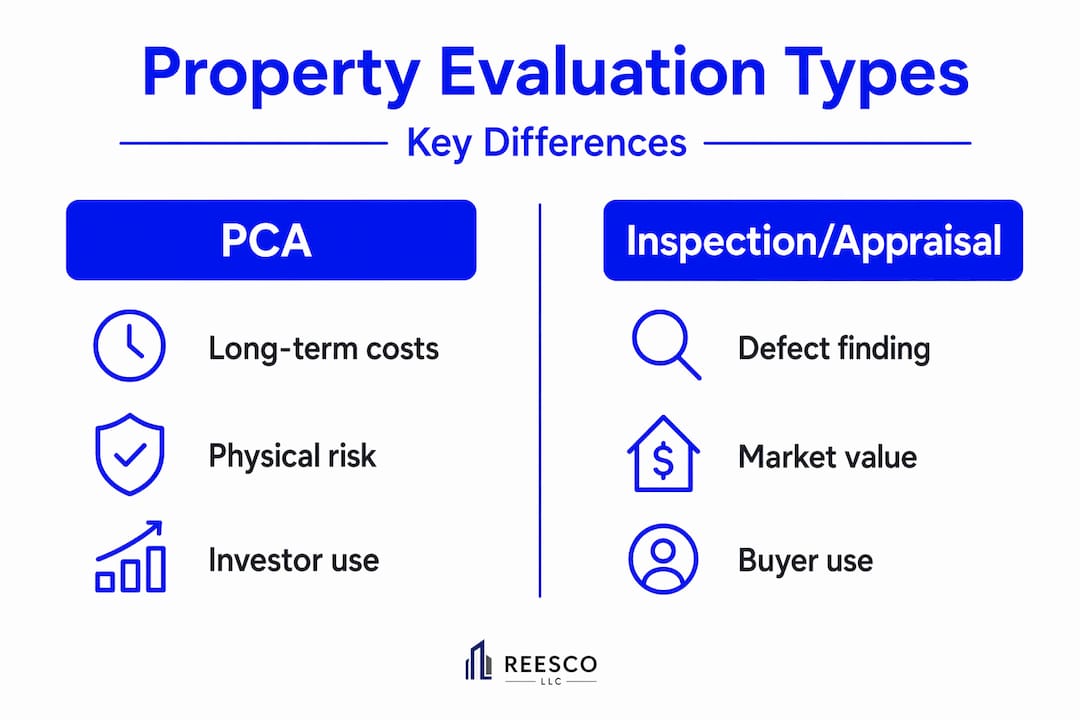

How PCAs compare to home inspections and appraisals

These three property evaluation tools serve different purposes and different audiences. Conflating them leads to gaps in due diligence.

| Evaluation Type | Primary Purpose | Typical User | Financial Output |

|---|---|---|---|

| Property Condition Assessment | Physical condition + capital cost projection | Commercial buyers, lenders, investors | 12-year cost tables, reserve estimates |

| Home Inspection | Identify visible defects at time of inspection | Residential buyers | Inspection report, repair list |

| Real Estate Appraisal | Determine market value | Buyers, lenders, sellers | Appraised value, market comparison |

A standard home inspection typically runs two to four hours and identifies defects in roughly 86% of residential properties, with roofing, electrical, and window issues topping the list. That’s useful for a homebuyer. It’s not sufficient for an investor acquiring a 24-unit apartment building.

An appraisal goes in the other direction. It establishes market value through comparable sales analysis but does not provide the building-level condition data or capital planning output that lenders and investors require for underwriting. Online valuation tools sit even further from reality. They use public records and algorithms that can’t account for a failing HVAC system or a roof with two years of service life left.

A PCA occupies a distinct space. It answers the question every serious investor should ask before closing: What will this property cost me over the next decade, and where are the hidden risks?

My take on PCAs in real estate investing

I’ve seen investors lose real money not because they skipped the assessment, but because they treated the report as a checklist rather than a financial instrument. They focused on the long list of minor findings, got reassured that “nothing major” appeared, and closed. Then two years later, the HVAC units reached end of service life on a 40-unit property all within the same season. That’s the domino effect in practice.

What I’ve learned from years of conducting these evaluations is that the most valuable part of any multifamily property inspection isn’t the list of what’s broken. It’s the pattern of what’s been neglected. Deferred maintenance rarely shows up as one catastrophic failure. It shows up as ten moderate issues concentrated in the same systems over the same years of ownership. That pattern tells you everything about how an asset has been managed.

My advice to investors is this: read the reserve table before you read the deficiency list. Understand what the property will demand from you financially over the next five to ten years. Then decide whether the purchase price reflects that reality. If it doesn’t, you have a negotiation. If the seller won’t move, you have an exit.

PCAs are evolving too. Standards are being updated, GSE requirements are tightening, and the expectation for digital documentation and photo evidence continues to grow. Working with firms that stay current on those standards protects you from compliance surprises at the worst possible time.

— Wes

Get a PCA that actually protects your investment

At Upchurch Inspection, we conduct property condition assessments for residential and commercial properties across the Mid-South, including Tennessee, Arkansas, Mississippi, and Southeast Missouri. Our reports go beyond surface-level observations. We deliver ASTM-compliant documentation with clear cost tables, system-by-system condition analysis, and the kind of financial detail lenders and investors rely on to make confident decisions.

Whether you’re evaluating a single commercial asset or managing a growing portfolio, our qualified inspectors bring the credentials and regional knowledge your transaction demands. If you need commercial buyer support or a thorough full property inspection, we’re ready to help. Contact Upchurch Inspection to schedule your assessment before your next closing.

FAQ

What is a property condition assessment?

A property condition assessment is a formal evaluation of a building’s physical condition, governed by the ASTM E2018-24 standard. It translates observed conditions into capital cost projections covering immediate repairs and a 12-year replacement reserve forecast.

How is a PCA different from a home inspection?

A home inspection identifies visible defects at the time of inspection, while a PCA goes further by projecting long-term capital costs and meeting the compliance requirements of lenders and GSEs for commercial and multifamily transactions.

When is a PCA required?

Lenders typically require a PCA for commercial property purchases and multifamily refinancing, especially when GSEs like Fannie Mae or Freddie Mac are involved. Investors also commission them voluntarily during due diligence to assess financial risk.

What does a PCA report include?

A compliant PCR includes an Immediate Repairs Table covering capital needs within 90 days, a Replacement Reserves Table projecting costs over 12 years, and an Opinion of Probable Costs tied to each major building system.

How long is a PCA valid?

Most lenders treat a PCA as valid for 12 months from the date of the site inspection. If a transaction extends beyond that window, the report may require a desk review or full update before closing.

Recommended

- Property Condition Assessments for Commercial Buyers | Upchurch Inspection

- Professional Property Condition Assessments (PCA) – Upchurch Inspection

- Investor Renovations vs. Owner Renovations: Key Differences Buyers Should Understand – Upchurch Inspection

- Commercial Property Inspection Guide: Confident Investments in 2026