Commercial real estate buyers often focus on income, location, tenant mix, lease terms, and financing.

Those things matter.

But once the property closes, the physical building starts telling the truth.

A commercial building can look profitable on paper while quietly carrying major capital risks. An aging roof, tired rooftop HVAC units, deteriorated plumbing, or failing parking lot can quickly turn a promising acquisition into an expensive ownership problem.

That is why commercial property due diligence should not be treated like a basic walkthrough.

The real question is not simply:

“Is the building in decent condition?”

The better question is:

“What major systems could force this buyer to spend serious money after closing?”

At Upchurch Inspection, we often look at commercial buildings through the lens of risk management and capital planning. The goal is not just to identify defects. The goal is to help buyers, investors, lenders, trustees, and property owners understand which conditions may affect future cost, operations, negotiations, and long-term ownership.

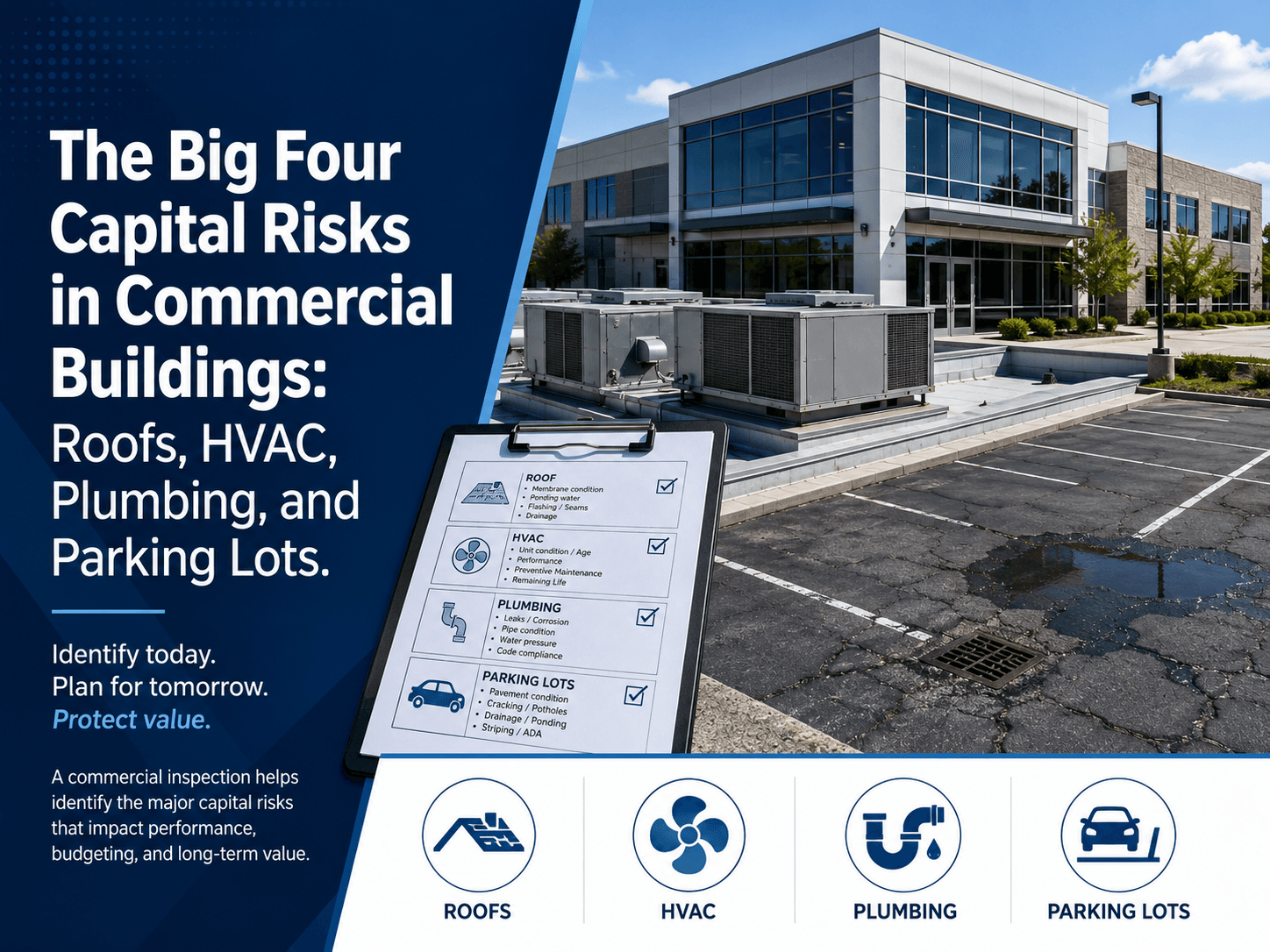

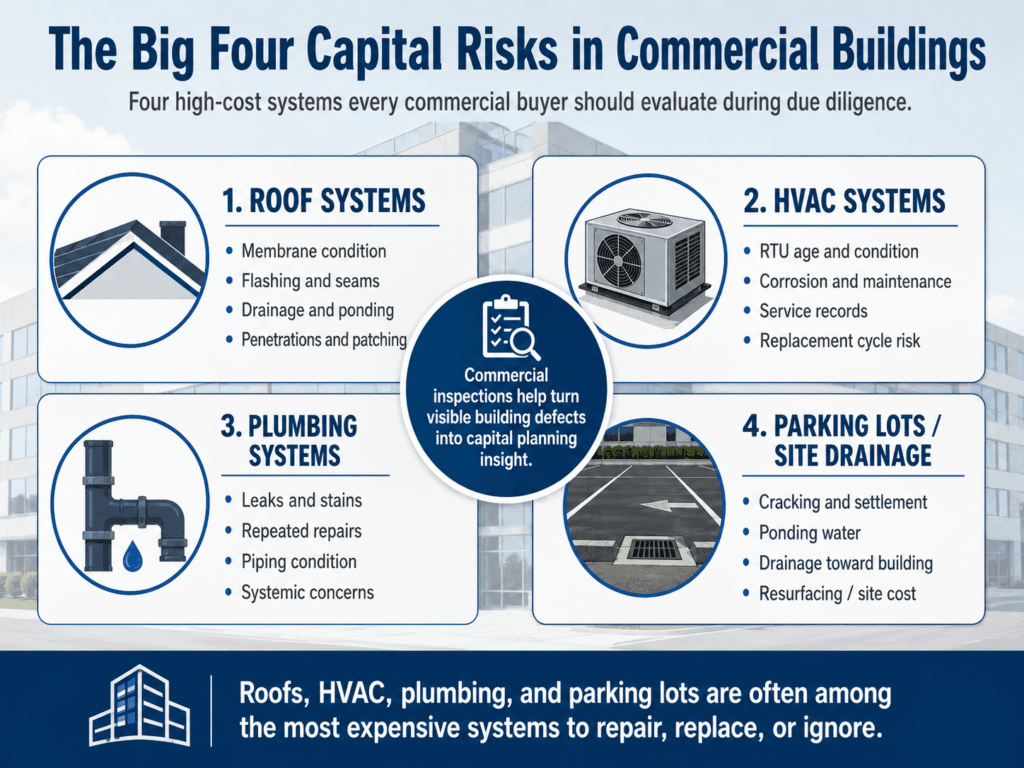

In many commercial buildings, four categories deserve special attention:

- Roof systems

- HVAC systems

- Plumbing systems

- Parking lots and site drainage

These are not the only systems that matter, but they are often among the most expensive to repair, replace, or ignore.

Why Capital Risk Matters in Commercial Property

A homebuyer may be concerned about repair costs.

A commercial buyer is concerned about repair costs, operational disruption, tenant complaints, liability exposure, lender concerns, insurance issues, lease obligations, and capital reserve planning.

That difference matters.

In commercial real estate, a defect is rarely just a defect. It can become a financial problem.

An old HVAC unit is not just a mechanical concern. It may affect tenant comfort, rental income, emergency service costs, and replacement budgeting.

A roof leak is not just a maintenance issue. It may affect interior finishes, inventory, electrical components, tenant operations, mold concerns, and insurance claims.

A deteriorated parking lot is not just ugly. It may create drainage issues, trip hazards, customer complaints, accessibility concerns, and major resurfacing costs.

A plumbing defect is not just a leak. In a multifamily building, restaurant, church, office, retail center, or institutional property, plumbing problems can become systemic.

Commercial due diligence should help the buyer understand what they are inheriting before those conditions become their responsibility.

1. Roof Systems: The First Major Capital Risk

Commercial roofs are one of the biggest concerns in a property acquisition.

They are expensive, they are often poorly maintained, and they can hide problems until damage has already spread into the building.

Unlike many residential roofs, commercial roofs are often low-slope or flat systems. These roofs depend heavily on proper drainage, membrane condition, flashing details, seams, penetrations, parapet walls, and roof-mounted equipment.

A commercial roof may not be actively leaking during a walkthrough, but that does not mean it is performing well.

Common Commercial Roof Concerns

During a commercial inspection or Property Condition Assessment, roof concerns may include:

- Ponding water

- Clogged drains

- Damaged roof membrane

- Open seams

- Deteriorated flashing

- Failed sealants

- Rusted metal components

- Damaged coping

- Improper patch repairs

- Soft or deteriorated areas

- Poor drainage slope

- Damaged roof penetrations

- Evidence of prior leaks

- Roof-mounted HVAC curbs that are not properly sealed

- Parapet wall deterioration

The roof should never be judged only by whether water is dripping inside on the day of inspection.

A roof can be near the end of its useful life and still appear “fine” to a casual observer.

That is the danger.

Why Roof Risk Is Financial Risk

Commercial roof replacement can be one of the largest capital expenses an owner faces.

Depending on the size, material, access, complexity, insulation, drainage, tear-off needs, and building use, roof work can be a major financial event.

Even repairs can add up quickly.

A buyer who does not understand the roof condition before closing may unknowingly inherit a large expense within the first few years of ownership.

That can affect:

- Purchase negotiations

- Capital reserves

- Insurance planning

- Tenant relations

- Maintenance budgets

- Lender confidence

- Long-term asset performance

In commercial property, the roof is not just a building component.

It is a financial exposure.

2. HVAC Systems: The Hidden Cost on the Roof

Commercial HVAC systems are often underestimated during due diligence.

The building may feel comfortable during the showing. Air may be coming out of the vents. The broker may say the systems are “working.”

That is not enough.

Commercial HVAC equipment can be expensive to repair, expensive to replace, and disruptive when it fails. Many commercial buildings rely on rooftop units, package units, split systems, boilers, chillers, or other mechanical systems that require more than a simple functional check.

A system can be operational and still be a major near-term capital concern.

Rooftop Units Deserve Special Attention

Rooftop units, commonly called RTUs, are common in commercial buildings throughout the Mid-South.

They sit outside in heat, humidity, rain, storms, temperature swings, and constant sun exposure. Over time, cabinets rust, coils get dirty, refrigerant line insulation deteriorates, electrical components age, condensate management suffers, and service life becomes a serious question.

During an assessment, visible concerns may include:

- Older equipment

- Rusted cabinets

- Damaged or missing insulation

- Dirty coils

- Damaged access panels

- Poor condensate drainage

- Evidence of repeated repairs

- Missing service records

- Unsafe electrical conditions

- Units not operating properly

- Inconsistent temperatures inside the building

- Poor maintenance access

- Equipment near or beyond expected service life

The key issue is not only whether the unit turns on.

The key issue is whether the buyer should expect meaningful HVAC expense after closing.

Multiple Units Multiply the Risk

One aging HVAC unit may be manageable.

A building with six aging rooftop units is a different conversation.

That is where commercial due diligence becomes important. Buyers need to understand whether HVAC concerns are isolated or part of a larger capital planning issue.

For example:

| HVAC Condition | Possible Buyer Concern |

|---|---|

| One older unit, others newer | Isolated replacement planning |

| Several units near the same age | Clustered capital expense risk |

| Poor maintenance across all units | Deferred maintenance concern |

| No service records available | Uncertain ownership risk |

| Units operating but visibly deteriorated | Near-term replacement budgeting |

This is the type of information commercial buyers need.

They are not just buying systems that work today.

They are buying the future cost of keeping those systems working.

3. Plumbing Systems: Isolated Defect or Systemic Problem?

Plumbing problems can be easy to underestimate.

A leak under one sink may be a simple repair. A staining pattern across multiple units, repeated drain issues, patched piping, corrosion, or water heater deterioration may suggest a larger problem.

In commercial properties, the question is often whether the plumbing issue is isolated or systemic.

That distinction matters.

Plumbing Risk by Property Type

Different commercial properties carry different plumbing concerns.

Multifamily Buildings

Older apartment buildings may have repeated leaks, aging supply lines, drain issues, water heater problems, failing shutoff valves, or repairs made unit by unit over many years.

A buyer should be asking:

- Are leaks isolated or repeated?

- Are plumbing materials consistent?

- Are there signs of chronic repairs?

- Are tenants reporting similar problems?

- Are multiple ceilings or cabinets stained?

- Are drain lines performing properly?

- Are water heaters near the end of useful life?

Restaurants and Food Service Spaces

Restaurants can create special plumbing concerns because of grease, heavy fixture use, floor drains, commercial sinks, restrooms, and high daily demand.

Concerns may include:

- Drainage problems

- Grease-related issues

- Fixture deterioration

- Leaks at commercial equipment

- Poor maintenance access

- Improper repairs

- Floor drain concerns

Churches, Schools, and Institutional Buildings

These properties may have restrooms, kitchens, classrooms, fellowship halls, laundry areas, and older piping serving multiple building sections.

The plumbing may not be heavily used every day, but when the building is active, demand can be high.

Office and Retail Buildings

Plumbing may appear limited, but restrooms, break rooms, janitor sinks, water heaters, and tenant improvements can still create concerns.

Poor tenant build-outs and amateur modifications are common in some commercial spaces.

Why Plumbing Defects Can Become Expensive

Plumbing failures can damage more than the plumbing system itself.

Leaks can affect:

- Flooring

- Ceilings

- Walls

- Cabinets

- Framing

- Insulation

- Electrical components

- Tenant spaces

- Indoor air quality

- Business operations

A commercial buyer needs to understand whether the observed plumbing concerns are minor repairs, deferred maintenance, or signs of a larger system approaching the end of its practical life.

This is especially important in older multifamily, mixed-use, institutional, and renovated commercial properties.

4. Parking Lots and Site Drainage: The Asset Outside the Building

Commercial buyers often pay close attention to the building and less attention to the site.

That can be a costly mistake.

Parking lots, sidewalks, curbs, exterior stairs, ramps, loading areas, retaining walls, stormwater features, and grading are all part of the asset.

They can also create major repair costs and liability concerns.

Common Parking Lot and Site Concerns

During commercial assessments, site concerns may include:

- Cracked asphalt

- Alligator cracking

- Failed patching

- Settlement

- Potholes

- Trip hazards

- Poor drainage

- Ponding water

- Damaged curbs

- Faded or missing striping

- Deteriorated sidewalks

- Damaged ramps

- Erosion

- Water movement toward the building

- Clogged drainage features

- Poorly maintained stormwater areas

A parking lot may still be usable while also approaching a significant repair cycle.

That distinction matters for capital planning.

Drainage Is a Mid-South Problem

In Memphis, West Tennessee, North Mississippi, Arkansas, Missouri, and the broader Mid-South, drainage deserves serious attention.

Heavy rain, clay soils, flat sites, older grading, and deferred maintenance can create water problems around commercial properties.

Poor drainage may contribute to:

- Foundation movement

- Slab moisture

- Crawlspace moisture

- Basement water intrusion

- Pavement deterioration

- Erosion

- Mold-related concerns

- Exterior wall damage

- Tenant complaints

- Roof drainage problems when downspouts discharge poorly

Drainage defects are often not dramatic during a showing.

But over time, water is one of the most destructive forces working against a building.

A commercial buyer should understand how water moves across the property before closing.

Parking Lots Can Become Liability Issues

A deteriorated parking lot is not only a repair issue.

It may also create safety and access concerns.

Trip hazards, uneven pavement, damaged walkways, poor lighting, ponding water, deteriorated stairs, and damaged curbs can all affect how people move through the property.

For retail, office, church, medical, daycare, multifamily, and institutional properties, the site is part of the public-facing experience.

If customers, tenants, visitors, employees, or congregation members use the property, site conditions matter.

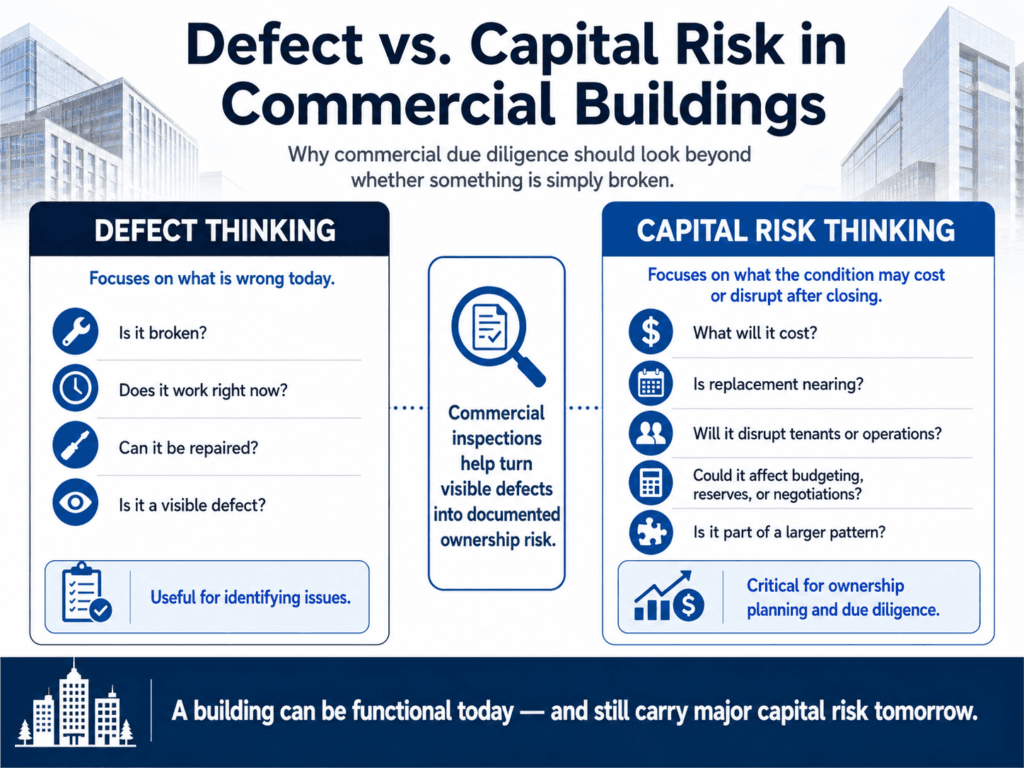

Why These Four Systems Belong in Every Commercial Due Diligence Conversation

Roofs, HVAC systems, plumbing, and parking lots have something in common:

They can all look manageable until they are not.

A buyer may walk through a building and see a functioning property.

But the assessment may reveal:

- The roof is near the end of its service life

- Multiple RTUs are aged and poorly maintained

- Plumbing defects appear in several areas

- The parking lot is deteriorated and holding water

- Drainage is moving toward the structure

- Repairs have been reactive instead of planned

That is where commercial due diligence becomes valuable.

The inspection helps turn vague risk into documented risk.

And documented risk can be used for:

- Negotiation

- Budgeting

- Specialist follow-up

- Capital reserve planning

- Ownership planning

- Lender discussions

- Board or investor review

- Deal evaluation

The point is not to kill a deal.

The point is to understand the deal.

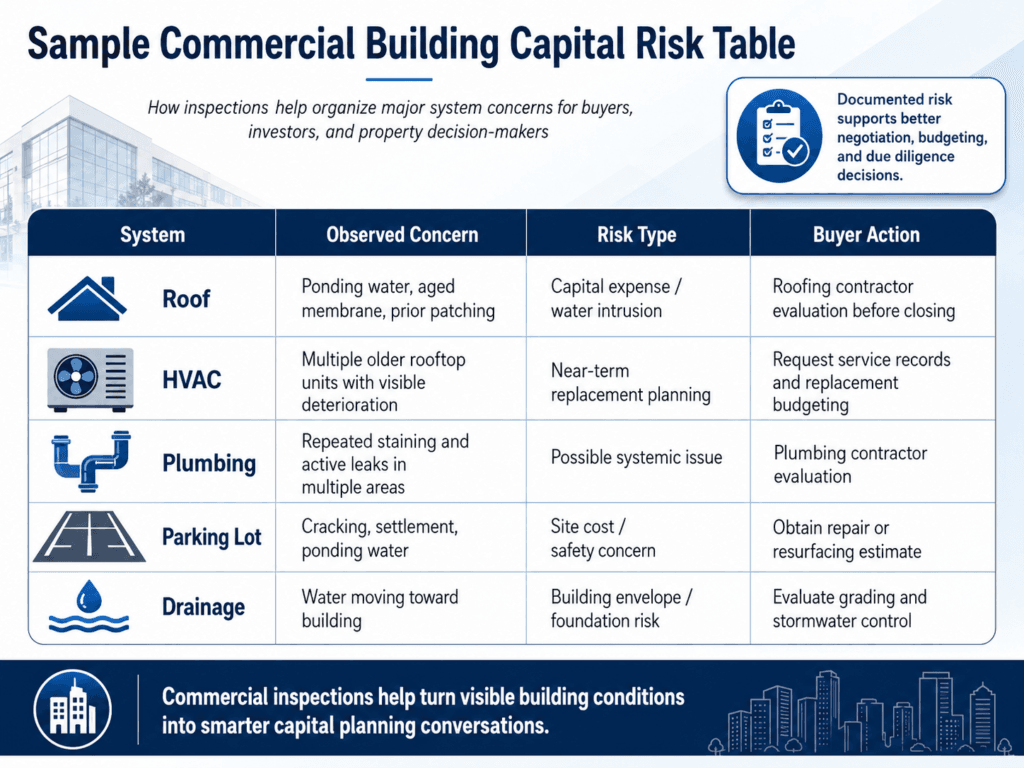

Sample Capital Risk Table

A commercial inspection or Property Condition Assessment may help organize findings in a way that supports decision-making.

For example:

| System | Observed Concern | Risk Type | Buyer Action |

|---|---|---|---|

| Roof | Ponding water, aged membrane, prior patching | Capital expense / water intrusion | Roofing contractor evaluation before closing |

| HVAC | Multiple older rooftop units with visible deterioration | Near-term replacement planning | Request service records and replacement budgeting |

| Plumbing | Repeated staining and active leaks in multiple areas | Possible systemic issue | Plumbing contractor evaluation |

| Parking Lot | Cracking, settlement, ponding water | Site cost / safety concern | Obtain repair or resurfacing estimate |

| Drainage | Water moving toward building | Building envelope / foundation risk | Evaluate grading and stormwater control |

This kind of framing helps buyers understand not only what was found, but why it matters financially.

Commercial Inspections Should Support the Business Decision

A commercial inspection should not be viewed as a generic checklist.

It should support the business decision behind the property.

That business decision may involve questions like:

- Does this property still make financial sense?

- Should the purchase price be renegotiated?

- Should repair credits be requested?

- Should the due diligence period be extended?

- Should specialists be brought in before closing?

- Should capital reserves be increased?

- Should a lender or board be notified of major concerns?

- Should the buyer walk away?

Not every defect changes a deal.

But some defects should change the buyer’s understanding of the deal.

That is the value of a properly scoped commercial assessment.

The Danger of Under-Scoping the Inspection

One mistake commercial buyers make is choosing an inspection scope that is too limited for the property.

A small retail space, large church campus, warehouse, office building, medical property, industrial facility, apartment complex, and mixed-use building should not all be approached the same way.

The scope should match:

- Building size

- Property type

- Age

- Complexity

- Intended use

- Buyer risk tolerance

- Lender requirements

- Time available during due diligence

- Whether cost opinions or reserve planning are needed

- Whether specialists should be involved

A low-cost walkthrough may be tempting, especially when closing costs are already adding up.

But the cheapest inspection may not answer the questions that matter.

Commercial buyers should be careful not to save a small amount upfront while missing a large capital expense after closing.

Local Conditions Matter

Commercial buildings in the Mid-South face conditions that can accelerate wear.

In our region, we commonly pay close attention to:

- Humidity

- Heavy rainfall

- Poor drainage

- Flat and low-slope roof systems

- Clay soils

- Aging HVAC equipment

- Older masonry buildings

- Long-term deferred maintenance

- Mixed-quality renovations

- Older multifamily plumbing

- Parking lot deterioration

- Crawlspace and moisture conditions where applicable

A commercial property assessment should consider how buildings actually age in the local environment.

That local context can make the difference between a generic report and a useful due diligence tool.

A commercial building may look functional during a walkthrough, but the real question is what major systems could require serious money after closing.

-Wes Upchurch, Upchurch Inspection

Final Thoughts

The biggest risks in commercial buildings are not always hidden.

Sometimes they are sitting in plain sight.

The roof is aging. The rooftop units are tired. The plumbing has been patched for years. The parking lot is cracking and holding water.

The question is whether the buyer understands what those conditions mean before closing.

Roofs, HVAC systems, plumbing, and parking lots are four of the most important capital risk areas in many commercial buildings. They affect cost, operation, safety, maintenance planning, tenant satisfaction, and long-term asset performance.

A commercial inspection or Property Condition Assessment should help buyers see beyond the surface and understand the financial liability attached to the property.

Because in commercial real estate, the building is not just a structure.

It is an asset.

And every asset carries risk.

Need a Commercial Property Inspection?

Upchurch Inspection provides commercial property inspections and Property Condition Assessments for investors, buyers, owners, lenders, trustees, and real estate professionals throughout the Mid-South.

We help clients evaluate commercial buildings with a focus on physical condition, deferred maintenance, major system risk, and practical decision-making before closing or major investment.

To discuss the right scope for your commercial property, contact Upchurch Inspection.